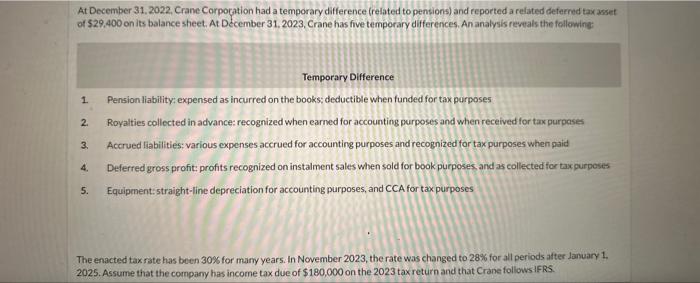

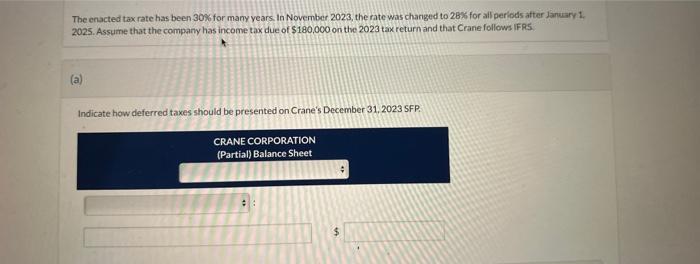

At December 31, 2022, Crane Corpocation had a temporary difference (related to pensions) and reported a refated deferned tax asset of $29.400 on its balance sheet. At December 31, 2023, Crane has five temporary differences, An analysis revels the following: Temporary Difference 1. Pension liability; expensed as incurred on the books; deductible when funded for tax parposes 2. Royalties collected in advance: recognized when earned for accounting purposes and when received for tax purposes 3. Accrued liabilities: various expenses accrued for accounting purposes and recognized for tax purposes when paid 4. Deferred gross profit: profits recognized on instalment sales when sold for book purposes, and as collected for tax purposies 5. Equipment: straight-line depreciation for accounting purposes, and CCA for tax purposes The enacted tax rate has been 30% for many years. In November 2023 , the rate was changed to 28% for all periods after lanuary 1 . 2025. Assume that the company has income tax due of $180,000 on the 2023 tax return and that Crane followsiFRS. The enacted taxrate has been 30% for many years. In November 2023, the rate was changed to 28% for all periods after January 1 . 2025. Assume that the company has income tax due of $180,000 on the 2023 tax return and that Crane follows if 95 (a) Indicate how deferred taxes should be presented on Crane's December 31, 2023 SFP. At December 31, 2022, Crane Corpocation had a temporary difference (related to pensions) and reported a refated deferned tax asset of $29.400 on its balance sheet. At December 31, 2023, Crane has five temporary differences, An analysis revels the following: Temporary Difference 1. Pension liability; expensed as incurred on the books; deductible when funded for tax parposes 2. Royalties collected in advance: recognized when earned for accounting purposes and when received for tax purposes 3. Accrued liabilities: various expenses accrued for accounting purposes and recognized for tax purposes when paid 4. Deferred gross profit: profits recognized on instalment sales when sold for book purposes, and as collected for tax purposies 5. Equipment: straight-line depreciation for accounting purposes, and CCA for tax purposes The enacted tax rate has been 30% for many years. In November 2023 , the rate was changed to 28% for all periods after lanuary 1 . 2025. Assume that the company has income tax due of $180,000 on the 2023 tax return and that Crane followsiFRS. The enacted taxrate has been 30% for many years. In November 2023, the rate was changed to 28% for all periods after January 1 . 2025. Assume that the company has income tax due of $180,000 on the 2023 tax return and that Crane follows if 95 (a) Indicate how deferred taxes should be presented on Crane's December 31, 2023 SFP