Answered step by step

Verified Expert Solution

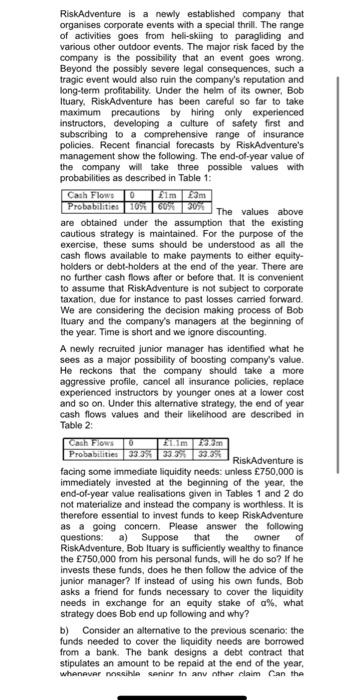

Question

1 Approved Answer

b) Consider an alternative to the previous scenario: the funds needed to cover the liquidity needs are borrowed from a bank. The bank designs a

b) Consider an alternative to the previous scenario: the funds needed to cover the liquidity needs are borrowed from a bank. The bank designs a debt contract that stipulates an amount to be repaid at the end of the year, whenever possible, senior to any other claim. Can the company secure the funds needed by financing the liquidity shock with debt? What strategy will the company follow then? Compare your answer to the solution obtained under equity finance and discuss.

b) Consider an alternative to the previous scenario: the funds needed to cover the liquidity needs are borrowed from a bank. The bank designs a debt contract that stipulates an amount to be repaid at the end of the year, whenever possible, senior to any other claim. Can the company secure the funds needed by financing the liquidity shock with debt? What strategy will the company follow then? Compare your answer to the solution obtained under equity finance and discuss.FM422 Corporate Finance: Amil Dasgupta

c) Suppose that in fact Bob Ituary immediately (and in a visible and public manner) rejected the risky strategy and fired the junior manager. True to its business model, RiskAdventure chose the safe strategy and negotiated with its bank a loan on that basis (i.e., the debt is negotiated after the risky strategy has been eliminated), to finance the 750,000. Consider now a situation that arises at some intermediate date, that is after the sums needed to cover the liquidity needs (750,000) have been invested and the operating strategy (the safe one) has been chosen, but before final cash flows are realized. It now appears that, at an extra cost of 50,000, all cash flows described in Table 1 can be increased by 54,000. Their respective chances are unaffected and remain as described in Table 1. Assume that unexpectedly Bob has access to some personal funds just equal to 50,000. If the sum of 750,000 was initially financed by debt, would Bob want to inject his own 50,000 in RiskAdventure? Comment on your result and describe what kind of negotiation could take place between the bank and Bob Ituary in relation to this further investment.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading For Beginners How To Generate Predictable Income And Make A Living Without Taking Big Risks Even If You Re A Complete Beginner

Authors: Greg Middleton

1st Edition

979-8866955046