Question

b) Price an interest swap that pays 0.5*face amount*(one-period spot rate - 8%) at period 1 and 2. c) If the market price for the

b) Price an interest swap that pays 0.5*face amount*(one-period spot rate - 8%) at period 1 and 2.

c) If the market price for the swap in (b) suggests a -100 bps OAS from the model, what is the market price?

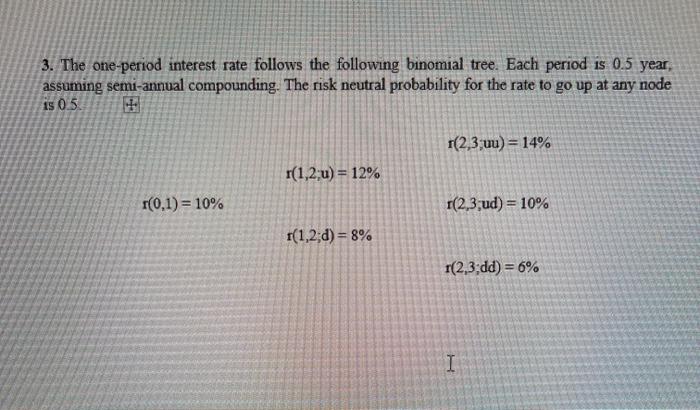

3. The one-period interest rate follows the following binomial tree. Each period is 0.5 year, assuming semi-annual compounding. The risk neutral probability for the rate to go up at any node 1s 0.5 r(2,3;uu) = 14% r(1,2;u) = 12% r(0,1)= 10% (2,3,ud) = 10% I(1,2;d) = 8% (2,3dd) = 6%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen

17th Edition

126001391X, 978-1260013917