Question

Background: You recently accepted the controller position for Java the Hut, a regional coffee chain. The owner informs you that a complete financial statement package

Background:

- You recently accepted the controller position for Java the Hut, a regional coffee chain.

- The owner informs you that a complete financial statement package will be required as part of a new bank loan compliance requirements ("covenants").

- Prior to your arrival, the company had one accountant and relied heavily on the auditors in the preparation of financial statements. With the new controller position, the expectation is that you will assume the preparation of financial statements.

- On your first day of work on April 1, 2018, the Java the Hut accountant informs you that there were a number of transactions in the first quarter of 2018 that she was unsure of the appropriate accounting.Consequently, she recorded the cash activity in the Other Assets - Holding account as a temporary holding account. The good news is that the Java the Hut accountant maintained excellent details of the various transactions and has a series of supporting schedules for you.

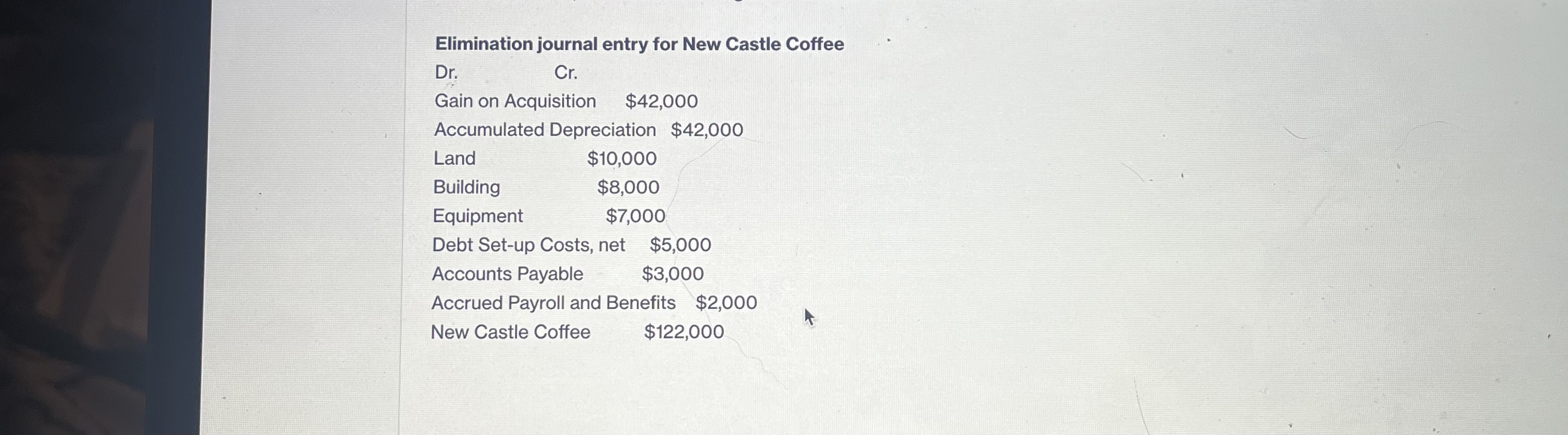

- The project reflects a "real-life" challenge in that you are responsible for accounting issues months following the actual transaction. In this case, an acquisition was completed on 1/1, and you are now responsible for acquisition accounting consolidated financial statements for the first three months (first quarter of 2018).Objective #3: Adjust Schedule 3 for Acquisition Values

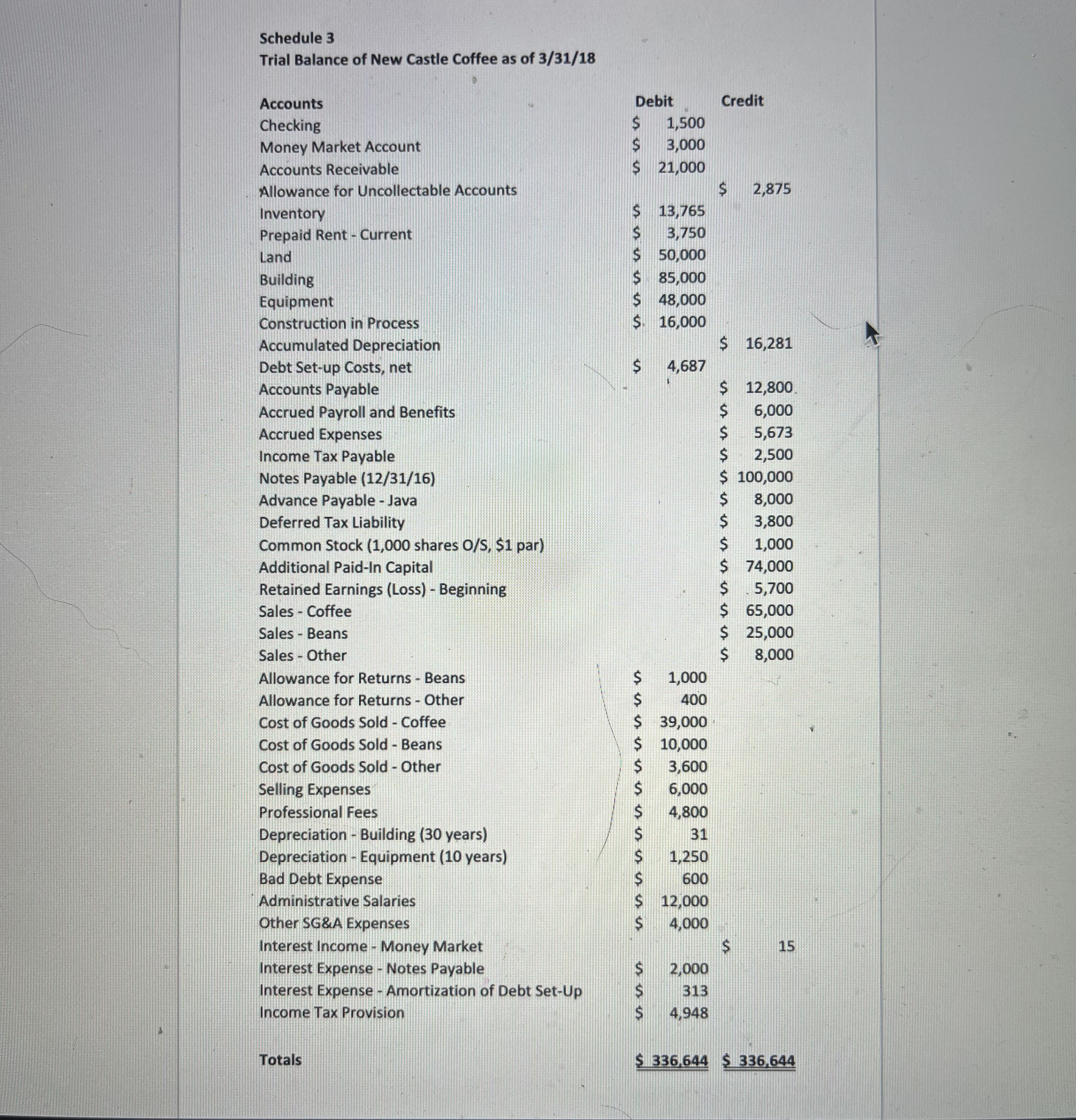

Because the project uses a situation you may encounter in practice, the reported results of New Castle Coffee on 3/31 included in Schedule 3 do not include any adjustments for the acquisition.Remember that the accounting department of New Castle Coffee would keep functioning as if the acquisition never occurred until new values were established. In practice, this is often a number of months following acquisition to complete the appropriate accounting.

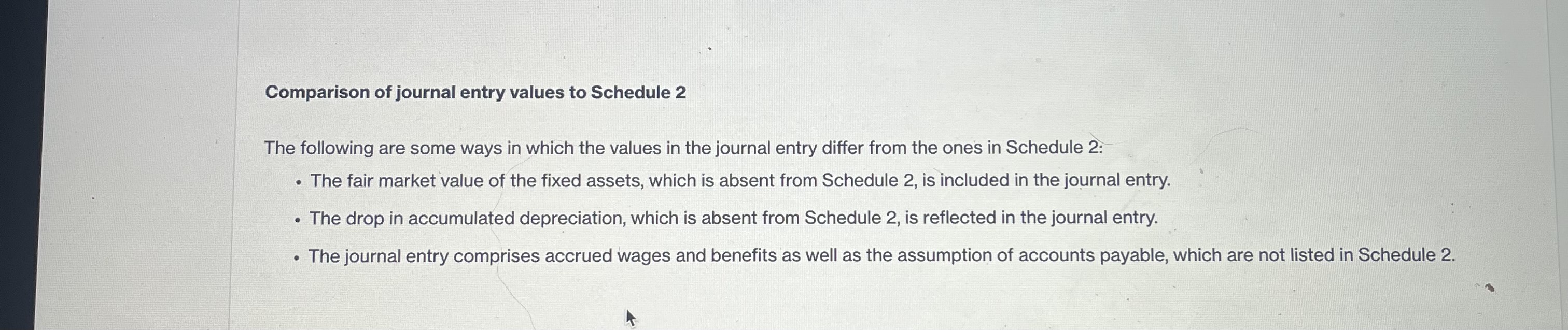

- Using only the Balance Sheet amounts in Schedule 3, calculate new balances by using the differences identified in #4 above and adding/subtracting to Schedule 3 amounts.

Only the Cash account through Retained Earnings are required to be adjusted.For example:

Land

Schedule 3 Reported $50,000

Increase in Acquisition Value + $10,000

Schedule 3 Adjusted $60,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accountancy And The Changing Landscape Of Integrated Reporting

Authors: Ioana Dragu

1st Edition

1522536221, 9781522536222