Answered step by step

Verified Expert Solution

Question

1 Approved Answer

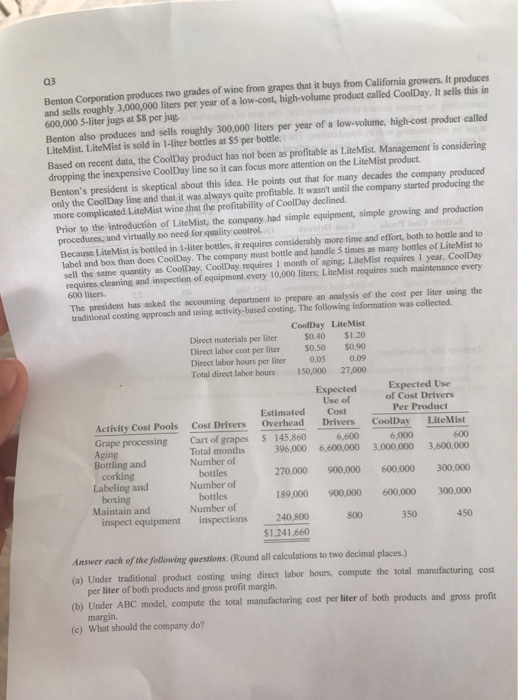

Benton Corporation produces two grades of wine from grapes that it buys from California growers. It produces and sells roughly 3.000.000 liters per year of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Key Concepts In Primary Science Audit And Subject Knowledge

Authors: Vivian Cooke, Colin Howard

1st Edition

1910391506, 978-1910391501