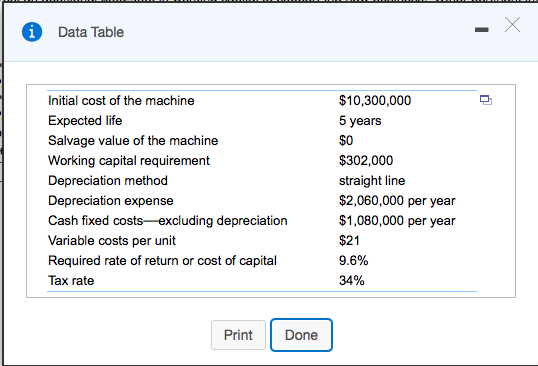

Blinkeria is considering introducing a new line of hand scanners that can be used to copy material and then download it into a personal computer. These scanners are expected to sell for an average price of $9898 each, and the company analysts performing the analysis expect that the firm can sell 100 comma 100,000 units per year at this price for a period of five years, after which time they expect demand for the product to end as a result of new technology. In addition, variable costs are expected to be $2121 per unit and fixed costs, not including depreciation, are forecast to be $1,080,000 per year. To manufacture this product, Blinkeria will need to buy a computerized production machine for $10.3 million that has no residual or salvage value, and will have an expected life of five years. In addition, the firm expects it will have to invest an additional $302,000 in working capital to support the new business.

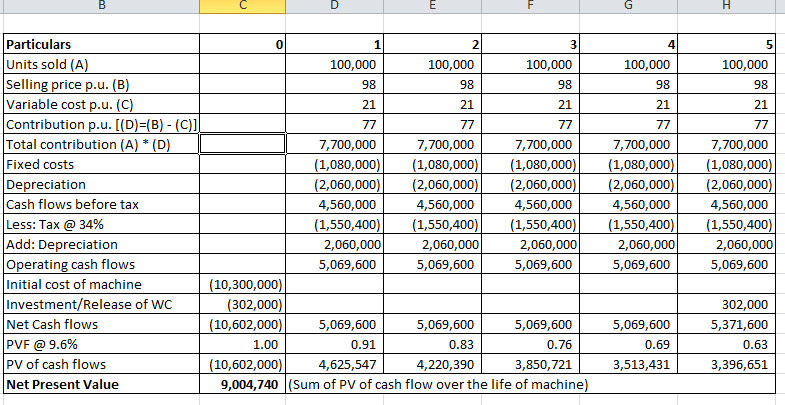

NPV=$9,004,740

e. The project's NPV to a(n)12 percent increase in the annual fixed operating costs will be $

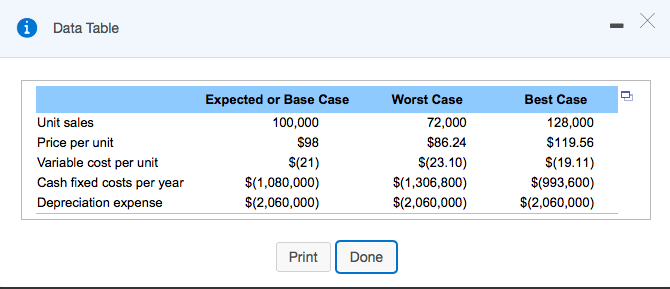

F. Use scenario analysis to evaluate the project's NPV under worst- and best-case scenarios for the project's value drivers. The values for the expected or base-case along with the worst- and best-case scenarios are listed here

A)

B) C)

C)

D)

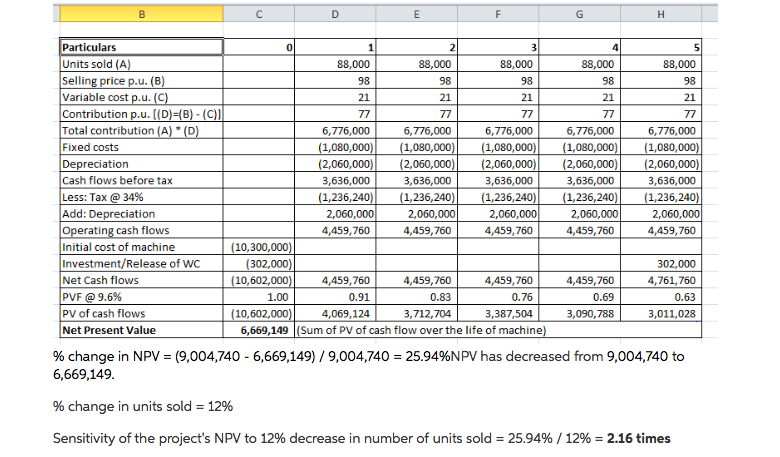

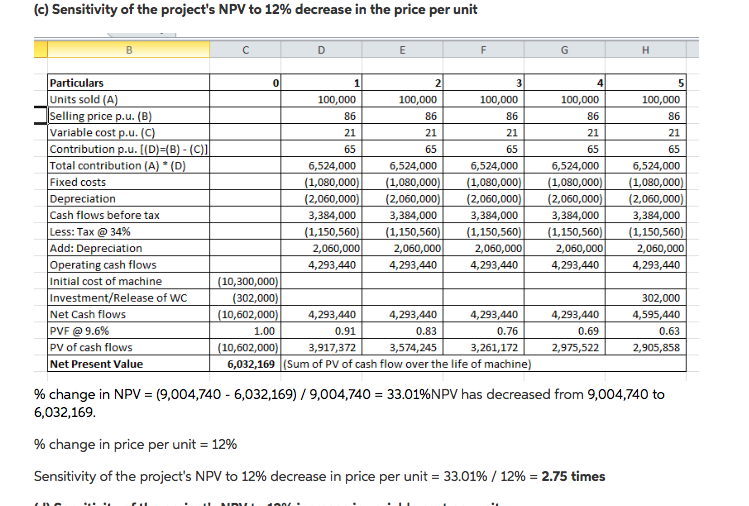

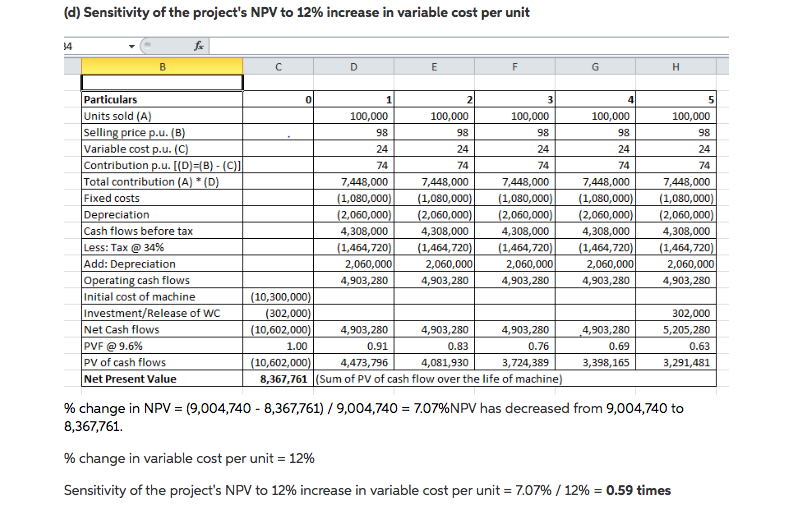

material and then download it into a personal computer. These scanners are expected to sell for an average price of $98 each, and the company analysts performing the analysis expect that the firm can sell 100,000 units per year at this price for a period of five years, after which time they expect demand for the product to end as a result of new technology. In addition, variable costs are expected to be $21 per unit and fixed costs, not including depreciation, are forecast to be $1,080,000 per year. To manufacture this product, Blinkeria will need to buy a computerized production machine for $10.3 million that has no residual or salvage value, and will have an expected life of five years. In addition, the firm expects it will have to invest an additional $302,000 in working capital to support the new business. Other pertinent information concerning the business venture is provided here: a. Calculate the project's NPV. b. Determine the sensitivity of the project's NPV to a(n) 12 percent decrease in the number of units sold. c. Determine the sensitivity of the project's NPV to a(n) 12 percent decrease in the price per unit. d. Determine the sensitivity of the project's NPV to a(n) 12 percent increase in the variable cost per unit. e. Determine the sensitivity of the project's NPV to a(n) 12 percent increase in the annual fixed operating costs. f. Use scenario analysis to evaluate the project's NPV under worst- and best-case scenarios for the project's value drivers. The values for the expected or base-case along with the worst, and hect.caca cronarinc are listed here: RR B 21 21 Particulars Units sold (A) Selling price p.u. (B) Variable cost p.u. (C) Contribution p.u. [(D)=(B)-(C) Total contribution (A) * (D) Fixed costs Depreciation Cash flows before tax Less: Tax @ 34% Add: Depreciation Operating cash flows Initial cost of machine Investment/Release of WC Net Cash flows PVF @ 9.6% PV of cash flows Net Present Value 21 3 100,000 100,000 100,000 98 98 98 21 77 77 77 7,700,000 7,700,000 7,700,000 (1,080,000) (1,080,000) (1,080,000)| (2,060,000) (2,060,000) (2,060,000) 4,560,000 4,560,000 4,560,000 (1,550,400) (1,550,400) (1,550,400) 2,060,000 2,060,000 2,060,000 5,069,600 5,069,600 5,069,600 (10,300,000) (302,000) (10,602,000)| 5,069,600 5,069,600 5,069,600 1.00 0.91 0.83 0.76 (10,602,000) 4,625,547 4,220,390 3,850,721 9,004,740 (Sum of PV of cash flow over the life of machine) 4 100,000 98 21 77 7,700,000 (1,080,000) (2,060,000) 4,560,000 (1,550,400) 2,060,000 5,069,600 100,000 98 21 77 7,700,000 (1,080,000) (2,060,000) 4,560,000 (1,550,400) 2,060,000 5,069,600 5,069,600 0.69 3,513,431 302,000 5,371,600 0.63 3,396,651 88.000 88,000 88,000 98 98 88,000 98 21 77 21 21 77 77 77 Particulars Units sold (A) Selling price p.u. (B) Variable cost p.u. (C) Contribution p.u. [(D)=(B) - (C) Total contribution (A) * (D) Fixed costs Depreciation Cash flows before tax Less: Tax @ 34% Add: Depreciation Operating cash flows Initial cost of machine Investment/Release of WC Net Cash flows PVF @ 9.6% PV of cash flows Net Present Value 6,776,000 6,776,000 6,776,000 (1,080,000) (1,080,000)| (1,080,000) (2,060,000) (2,060,000)| (2,060,000) 3,636,000 3,636,000 3,636,000 (1,236,240)| (1,236,240) (1,236,240) 2,060,000 2,060,000 2,060,000 4,459,760 1 4,459,760 4,459,760 (10,300,000) (302,000) (10,602,000) 4,459,760 4,459,760 4,459,760 1.00 0.91 0.83 0.76 (10,602,000) 4,069,124 3,712,704 3,387,504 6,669,149 (Sum of PV of cash flow over the life of machine) 88,000 98 21 77 6,776,000 (1,080,000)| (2,060,000)| 3,636,000 (1,236,240)| 2,060,000 4,459,760 6,776,000 (1,080,000) (2,060,000) 3,636,000 (1,236, 240) 2,060,000 4,459,760 4 302,000 4,761,760 0.63 3,011,028 ,459,760 0.69 3,090,788 91 % change in NPV = (9,004,740 - 6,669,149) / 9,004,740 = 25.94%NPV has decreased from 9,004,740 to 6,669,149. % change in units sold = 12% Sensitivity of the project's NPV to 12% decrease in number of units sold = 25.94% / 12% = 2.16 times (c) Sensitivity of the project's NPV to 12% decrease in the price per unit F G 100,000 86 21 65 Particulars Units sold (A) Selling price p.u. (B) Variable cost p.u. (C) Contribution p.u. [(D)=(B) - (c)] Total contribution (A) * (D) Fixed costs Depreciation Cash flows before tax Less: Tax @ 34% Add: Depreciation Operating cash flows Initial cost of machine Investment/Release of WC Net Cash flows PVF @ 9.6% PV of cash flows Net Present Value 2 100,000 100,000 100,000 86 86 86 21 21 21 65 65 65 6,524,000 6,524,000 6,524,000 (1,080,000) (1,080,000) (1,080,000) (2,060,000)| (2,060,000)| (2,060,000)| 3,384,000 3,384,000 3,384,000 1 (1,150,560) (1,150,560) (1,150,560) 2,060,000 2,060,000 2,060,000 4,293,440 4,293,440 4,293,440 (10,300,000) (302,000) (10,602,000) 4,293,440 4,293,440 4,293,440 1.00 0.91 0.83 0.76 (10,602,000) 3,917,372 3,574,245 3,261,172 6,032,169 (Sum of PV of cash flow over the life of machine) 4 100,000 86 21 65 6,524,000 (1,080,000) (2,060,000) 3,384,000 (1,150,560) 2,060,000 4,293,440 6,524,000 (1,080,000) (2,060,000) 3,384,000 (1,150,560) 2,060,000 4,293,440 4,293,440 0.69 2,975,522 302,000 4,595,440 0.63 2,905,858 % change in NPV = (9,004,740 - 6,032,169) / 9,004,740 = 33.01%NPV has decreased from 9,004,740 to 6,032,169. % change in price per unit = 12% Sensitivity of the project's NPV to 12% decrease in price per unit = 33.01% / 12% = 2.75 times (d) Sensitivity of the project's NPV to 12% increase in variable cost per unit 14 fa C D E F G H 74 74 Particulars Units sold (A) Selling price p.u. (B) Variable cost p.u. (C) Contribution p.u. [(D =(B) - (C) Total contribution (A) * (D) Fixed costs Depreciation Cash flows before tax Less: Tax @ 34% Add: Depreciation Operating cash flows Initial cost of machine Investment/Release of WC Net Cash flows PVF @ 9.6% PV of cash flows Net Present Value 100,000 100,000 100,000 98 98 98 24 24 24 74 7,448,000 7,448,000 7,448,000 (1,080,000) (1,080,000) (1,080,000) (2,060,000) (2,060,000) (2,060,000)| 4,308,000 4,308,000 4,308,000 (1,464,720) (1,464,720) (1,464,720) 2,060,000 2,060,000 2,060,000 4,903,280 4,903,280 4,903,280 (10,300,000) (302,000) (10,602,000) 4,903,280 4,903,280 4,903,280 1.00 0.91 0.83 0.76 (10,602,000) 4,473,796 4,081,930 3 ,724,389 8,367,761 (Sum of PV of cash flow over the life of machine) 100,000 98 24 74 7,448,000 (1,080,000) (2,060,000)| 4,308,000 (1,464,720)| 2,060,000 4,903,280 100,000 98 24 74 7,448,000 (1,080,000) (2,060,000) 4,308,000 (1,464,720) 2,060,000 4,903,280 4,903,280 0.69 3,398,165 302,000 5,205,280 0.63 3,291,481 % change in NPV = (9,004,740 - 8,367,761) / 9,004,740 = 7.07%NPV has decreased from 9,004,740 to 8,367,761 % change in variable cost per unit = 12% Sensitivity of the project's NPV to 12% increase in variable cost per unit = 7.07% / 12% = 0.59 times