Answered step by step

Verified Expert Solution

Question

1 Approved Answer

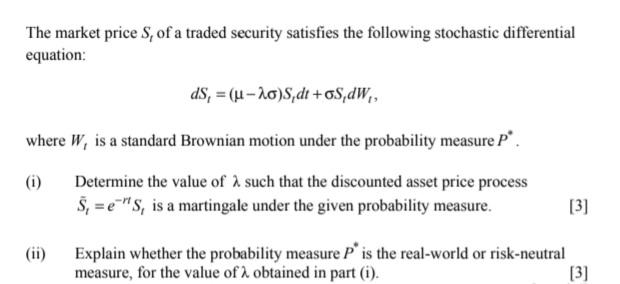

The market price S, of a traded security satisfies the following stochastic differential equation: dS, (u-o)S,dt+S,dW, where W, is a standard Brownian motion under

The market price S, of a traded security satisfies the following stochastic differential equation: dS, (u-o)S,dt+S,dW, where W, is a standard Brownian motion under the probability measure P*. (i) Determine the value of such that the discounted asset price process S = eS, is a martingale under the given probability measure. [3] (ii) Explain whether the probability measure P' is the real-world or risk-neutral measure, for the value of obtained in part (i). [3]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To calculate the cost of capital components and the Weighted Average Cost of Capital WACC for Marriott Hotels International we need several inputs and ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost management a strategic approach

Authors: Edward J. Blocher, David E. Stout, Gary Cokins

5th edition

73526940, 978-0073526942