Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Calculate the investment proportions , expected return and volatility of the optimal risky portfolio of the two risky funds. (8 points) A global equity fund

Calculate the investment proportions, expected return and volatility of the optimal risky portfolio of the two risky funds. (8 points)

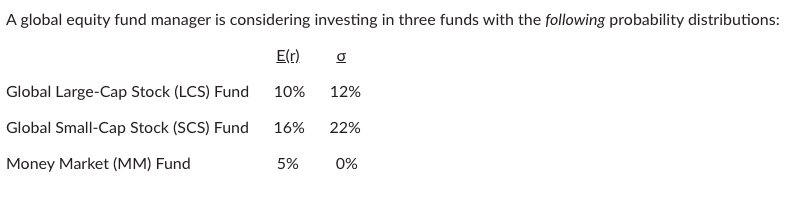

A global equity fund manager is considering investing in three funds with the following probability distributions: E(r) o 10% 12% Global Large-Cap Stock (LCS) Fund Global Small-Cap Stock (SCS) Fund 16% 22% Money Market (MM) Fund 5% 0% A global equity fund manager is considering investing in three funds with the following probability distributions: E(r) o 10% 12% Global Large-Cap Stock (LCS) Fund Global Small-Cap Stock (SCS) Fund 16% 22% Money Market (MM) Fund 5% 0%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to Finance Markets, Investments and Financial Management

Authors: Ronald W. Melicher, Edgar A. Norton

16th edition

1119398282, 978-1-119-3211, 1119321115, 978-1119398288