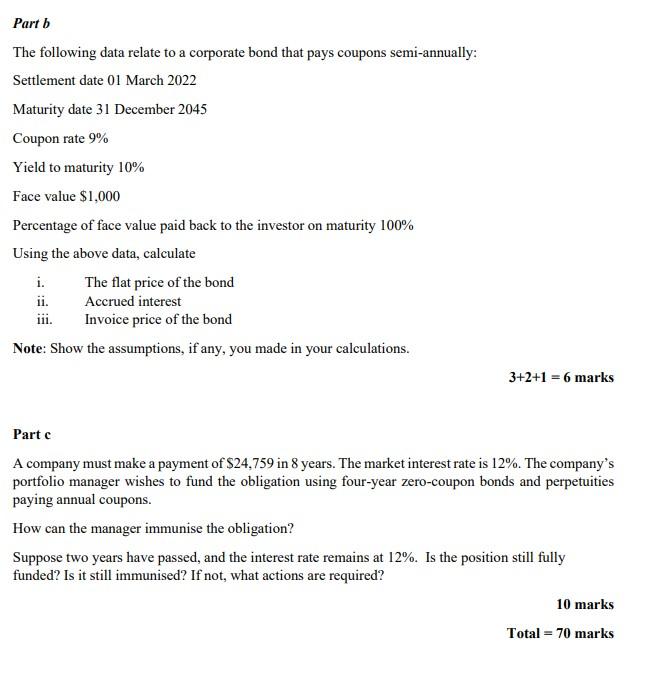

Question

Can an expert pls give me an ansere thank you You are the portfolio manager of a large company that invests in many securities, including

Can an expert pls give me an ansere thank you

You are the portfolio manager of a large company that invests in many securities, including corporate bonds. You have been assigned the task of bond portfolio management. You are provided with the following data about bonds:

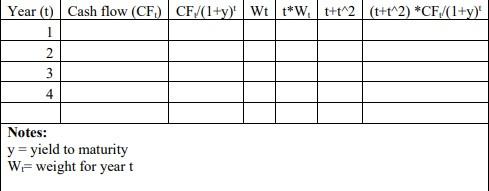

The maturity period is four years

Coupon rate 10%

Par value $1,000

Coupons on bonds are paid annually

Yield to maturity of bonds 11%

i) Using the above data, fill in the blanks in the following table

See the lecture notes for formulae ii)

Based on the calculations in part i, calculate the modified duration and convexity of the bond

iii) Using the modified duration, calculate the change in bond price in dollars when yield to maturity changes by two per cent

iv) Using the convexity, calculate the change in bond price in dollars when yield to maturity changes by two per cent

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing The Audit Function A Corporate Audit Department Procedures Guide

Authors: Michael P. Cangemi

2nd Edition

0471012556, 978-0471012559