Answered step by step

Verified Expert Solution

Question

1 Approved Answer

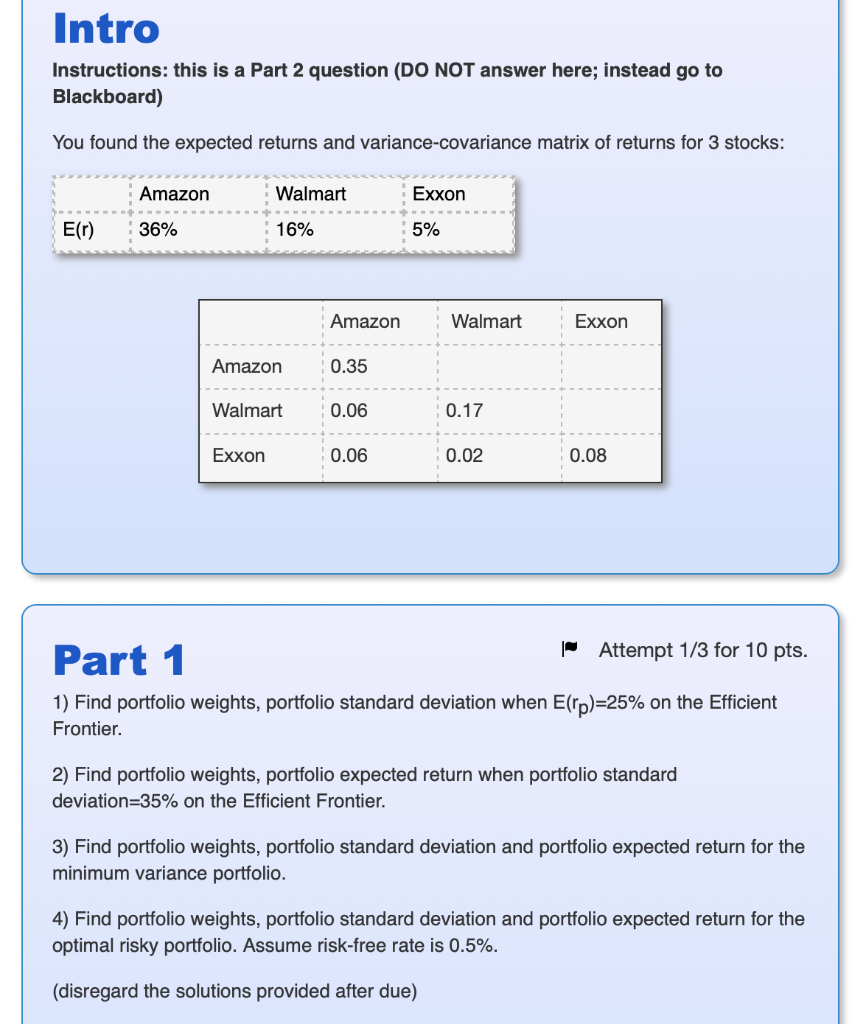

can be done using solver in excel please. Intro Instructions: this is a Part 2 question (DO NOT answer here; instead go to Blackboard) You

can be done using solver in excel please.

Intro Instructions: this is a Part 2 question (DO NOT answer here; instead go to Blackboard) You found the expected returns and variance-covariance matrix of returns for 3 stocks: Amazon Walmart Exxon E() 36% 16% 5% Amazon Walmart Exxon Amazon 0.35 Walmart 0.06 0.17 Exxon 0.06 0.02 0.08 Part 1 Attempt 1/3 for 10 pts. 1) Find portfolio weights, portfolio standard deviation when E(rp)=25% on the Efficient Frontier. 2) Find portfolio weights, portfolio expected return when portfolio standard deviation=35% on the Efficient Frontier. 3) Find portfolio weights, portfolio standard deviation and portfolio expected return for the minimum variance tfolio. 4) Find portfolio weights, portfolio standard deviation and portfolio expected return for the optimal risky portfolio. Assume risk-free rate is 0.5%. (disregard the solutions provided after due) Intro Instructions: this is a Part 2 question (DO NOT answer here; instead go to Blackboard) You found the expected returns and variance-covariance matrix of returns for 3 stocks: Amazon Walmart Exxon E() 36% 16% 5% Amazon Walmart Exxon Amazon 0.35 Walmart 0.06 0.17 Exxon 0.06 0.02 0.08 Part 1 Attempt 1/3 for 10 pts. 1) Find portfolio weights, portfolio standard deviation when E(rp)=25% on the Efficient Frontier. 2) Find portfolio weights, portfolio expected return when portfolio standard deviation=35% on the Efficient Frontier. 3) Find portfolio weights, portfolio standard deviation and portfolio expected return for the minimum variance tfolio. 4) Find portfolio weights, portfolio standard deviation and portfolio expected return for the optimal risky portfolio. Assume risk-free rate is 0.5%. (disregard the solutions provided after due)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Financial Communication And Investor Relations

Authors: Alexander V. Laskin

1st Edition

1119240786, 978-1119240785