Answered step by step

Verified Expert Solution

Question

1 Approved Answer

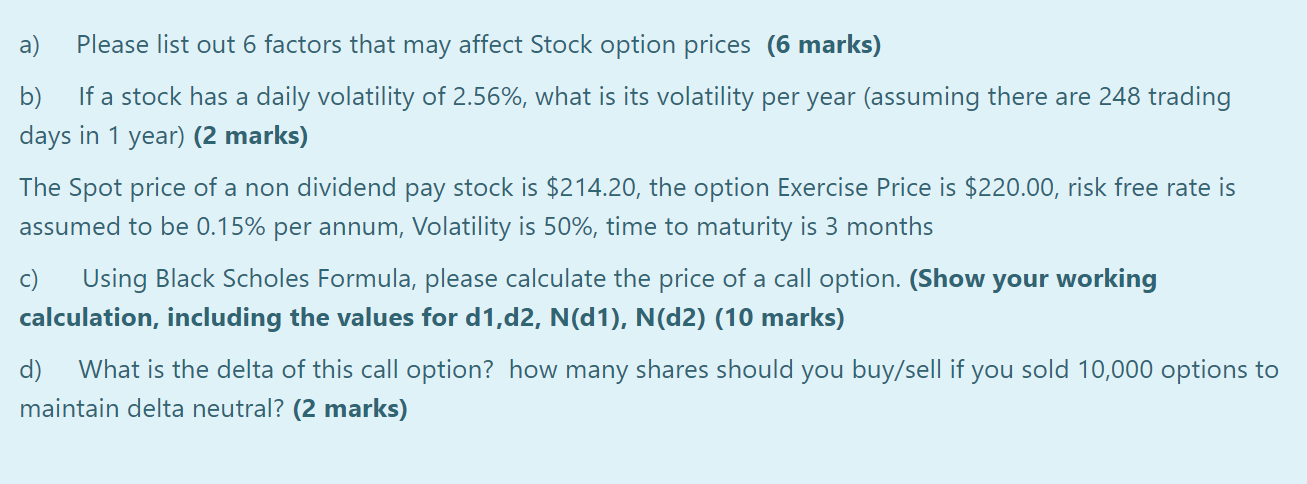

Can someone help me to slove this question? a) Please list out 6 factors that may affect Stock option prices (6 marks) b) If a

Can someone help me to slove this question?

Can someone help me to slove this question?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: James D. Stice, Earl K. Stice, Fred Skousen

16th Edition

324376375, 0324375743I, 978-0324376371, 9780324375749, 978-0324312140