Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Can you give me the whole work to solve the problem instead of an answer Berkshire Hathaway (ticker: BRK/A) S&P 500 Index (ticker: SPX) NASDAQ

Can you give me the whole work to solve the problem instead of an answer

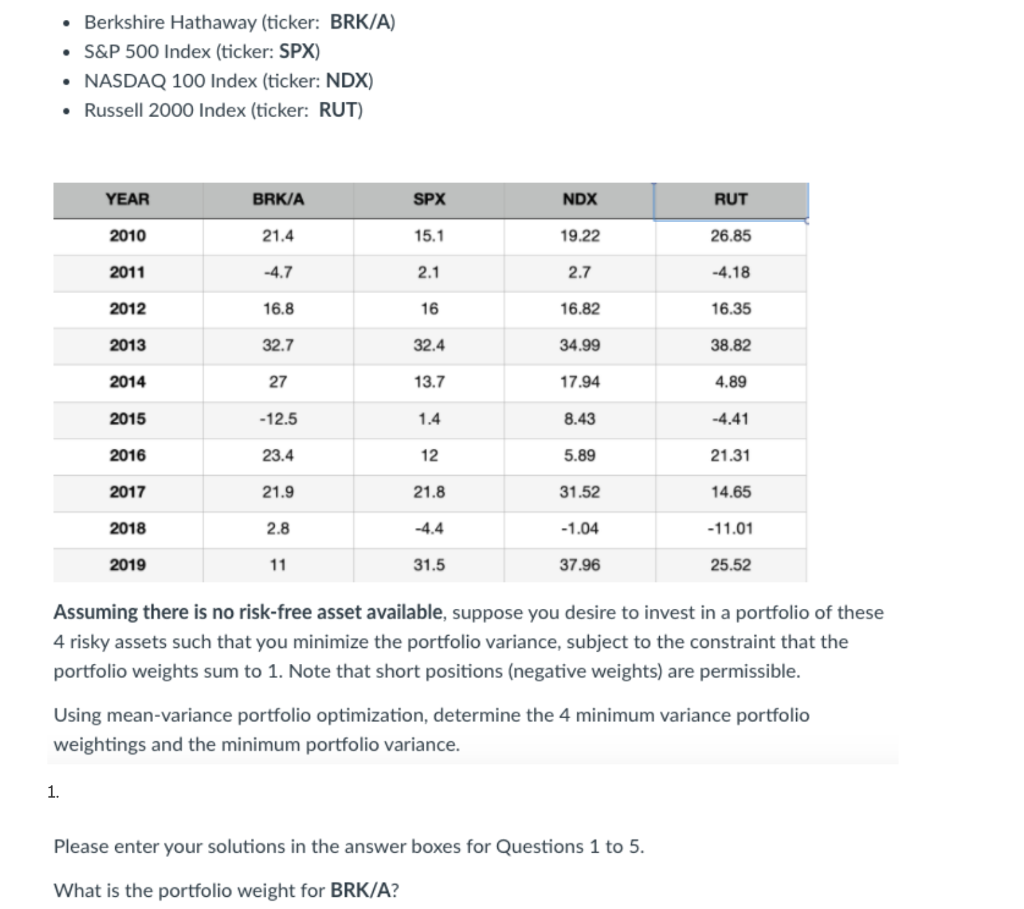

Berkshire Hathaway (ticker: BRK/A) S&P 500 Index (ticker: SPX) NASDAQ 100 Index (ticker: NDX) Russell 2000 Index (ticker: RUT) YEAR BRK/A SPX NDX RUT 2010 21.4 15.1 19.22 26.85 2011 -4.7 2.1 2.7 -4.18 2012 16.8 16 16.82 16.35 2013 32.7 32.4 34.99 38.82 2014 27 13.7 17.94 4.89 2015 - 12.5 1.4 8.43 -4.41 2016 23.4 12 5.89 21.31 2017 21.9 21.8 31.52 14.65 2018 2.8 -4.4 -1.04 -11.01 2019 11 31.5 37.96 25.52 Assuming there is no risk-free asset available, suppose you desire to invest in a portfolio of these 4 risky assets such that you minimize the portfolio variance, subject to the constraint that the portfolio weights sum to 1. Note that short positions (negative weights) are permissible. Using mean-variance portfolio optimization, determine the 4 minimum variance portfolio weightings and the minimum portfolio variance. 1. Please enter your solutions in the answer boxes for Questions 1 to 5. What is the portfolio weight for BRK/A? Berkshire Hathaway (ticker: BRK/A) S&P 500 Index (ticker: SPX) NASDAQ 100 Index (ticker: NDX) Russell 2000 Index (ticker: RUT) YEAR BRK/A SPX NDX RUT 2010 21.4 15.1 19.22 26.85 2011 -4.7 2.1 2.7 -4.18 2012 16.8 16 16.82 16.35 2013 32.7 32.4 34.99 38.82 2014 27 13.7 17.94 4.89 2015 - 12.5 1.4 8.43 -4.41 2016 23.4 12 5.89 21.31 2017 21.9 21.8 31.52 14.65 2018 2.8 -4.4 -1.04 -11.01 2019 11 31.5 37.96 25.52 Assuming there is no risk-free asset available, suppose you desire to invest in a portfolio of these 4 risky assets such that you minimize the portfolio variance, subject to the constraint that the portfolio weights sum to 1. Note that short positions (negative weights) are permissible. Using mean-variance portfolio optimization, determine the 4 minimum variance portfolio weightings and the minimum portfolio variance. 1. Please enter your solutions in the answer boxes for Questions 1 to 5. What is the portfolio weight for BRK/AStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Financial Crisis Implications For Research And Teaching

Authors: Ted Azarmi, Wolfgang Amann

1st Edition

3319205870, 978-3319205878