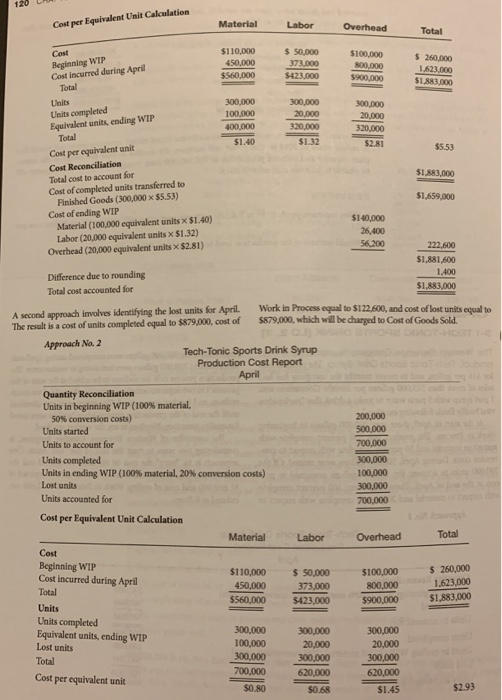

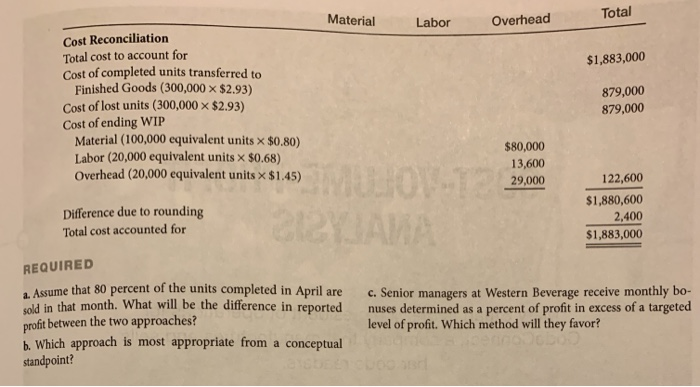

CASE 3-1 1 TECH-TONIC SPORTS DRINK [LO 2, 3 Western Beverage Company is marketing a new conversion costs: 300,000 gallons were completed during April and, The oroduct, Tech-Tonic Sports Drink Syrup. The product sells unfortunately. 300,000 gallons were lost owing to worker error. The or $16 per gallon, and in recent months the company has had production process calls for sodium to be added at the start of the ales of more than 525,000 gallons per month. Consumers mix process. On two separate occasions, a new worker added too much part syrup with 5 parts water to make a drink that "replenishes sodium, and batches were ruined. The errors were not identified vital bodily fluids following exertion." until the end of the production process when batches were tested At the start of April, there were 200,000 gallons in beginning for quality assurance. Needless to say, the worker was fired Work in Process. The product was 100 percent complete with The controller of Western Beverage, Gunther Bergman,s to material and 50 percent complete with respect to con- considering two ways to treat the cost of the "lost" units. One yersion costs. During April, 500,000 gallons were started. of the approach is to "bury" the cost in the units completed and the 200,000 units to account for, 100,000 gallons remained in pro units in process. This would result in cost of units completed of cess at the end of April. These units were 100 percent complete $1,669,000 and cost of ending Work in Process of $222,600 cal- with respect to material and 20 percent complete with respect to culated as follows. Approach No.I Tech-Tonic Sports Drink Syrup Production Cost Report April Quantity Reconciliation Units in beginning WIP (100% material, 50% conversion costs) Units started Units to account for 200,000 500,000 700,000 300,000 100,000 300,000 700,000 Units completed Units in ending WIP ( i 00% material, 20% conversion costs) Lost units Units accounted for 20L Cost per Equivalent Unit Calculation Material 110,000 50,000 373,000 $423,000 $100,000 Beginning WIP Cost incurred during April $ 260,000 1623,000 $1,883,000 450,000 $900,000 Total Units completed Equivalent units, ending WIP 20,000 320,000 100,000 20,000 320,000 $2.81 Total Cost per equivalent unit Total cost to account for $1.40 $1.32 $5.53 $1,883,000 $1,659,000 Cost of completed units transferred to Finished Goods (300,000 x $5.53) Cost of ending WIP $140,000 26,400 Material (100,000 equivalent units x $1.40) Labor (20,000 equivalent units x $1.32) Overhead (20,000 equivalent units $2.81) Difference due to rounding Total cost accounted for $1,881,600 1,400 $1,883,000 A second approach involves identifying the lost units for April. Work in Process equal to $122,600, and cost of lost units equal to The resalt is a cost of units completed equal to $879,000, cost of $879,000, which will be charged to Cost of Goods Sold. Approach No. 2 Tech-Tonic Sports Drink Syrup Production Cost Report April Quantity Reconciliation Units in beginning VVIP (100% material. 50% conversion costs) Units started Units to account for 700,000 Units completed Units in ending WIP (100% material, 20% conversion costs) Lost units Units accounted for 100,000 300,000 Cost per Equivalent Unit Calculation Material Labor Overhead Total Cost Beginning WIP Cost incurred during April Total Units Units completed Equivalent units, ending WIP Lost units Total 110,000 $ 50,000$100,000 50,000 373000 800,000 $560,000 $423,000 260,000 1,623,000 $900,000 $ 883,000 300,000 100,000 300,000 300,000 20,000 300,000 620,000 $1.45 300,000 Cost per equivalent unit $0.80 $2.93 Labor Overhead Total Cost Reconciliation Total cost to account for Cost of completed units transferred to $1,883,000 Finished Goods (300,000 x $2.93) Cost of lost units (300,000 x $2.93) Cost of ending WIP 879,000 879,000 Material (100,000 equivalent units $0.30) Labor (20,000 equivalent units x $0.68) Overhead (20,000 equivalent units x $1.45) $80,000 13,600 29,000 22,600 $1,880,600 2,400 $1,883,000 Difference due to rounding Total cost accounted for REQUIRED a. Assume that 80 percent of the units completed in April are c. Senior managers at Western Beverage receive monthly bo- sold in that month. What will be the difference in reported nuses determined as a percent of profit in excess of a targeted profit between the two approaches? level of profit. Which method will they favor? s vepchil R1scpteal standpoint