Answered step by step

Verified Expert Solution

Question

1 Approved Answer

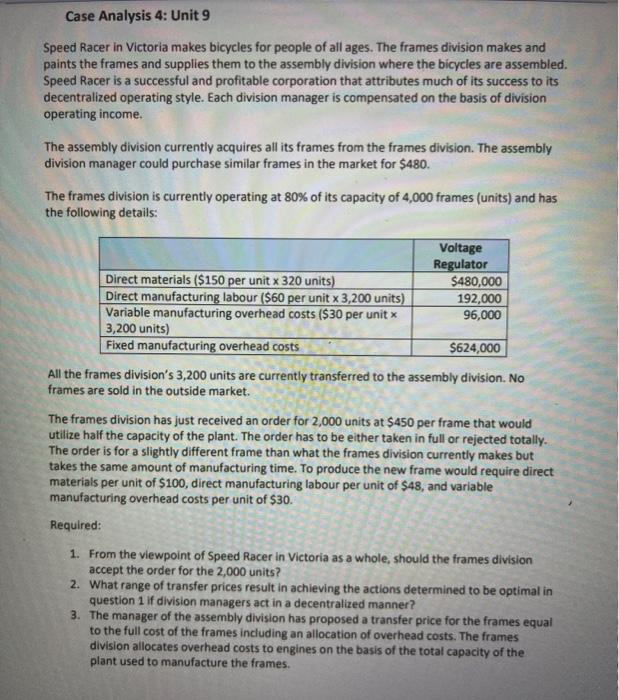

Case Analysis 4: Unit 9 Speed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistical Techniques For Analytical Review In Auditing

Authors: Kenneth W. Stringer, Trevor R. Stewart

1st Edition

047186076X, 978-0471860761