Question

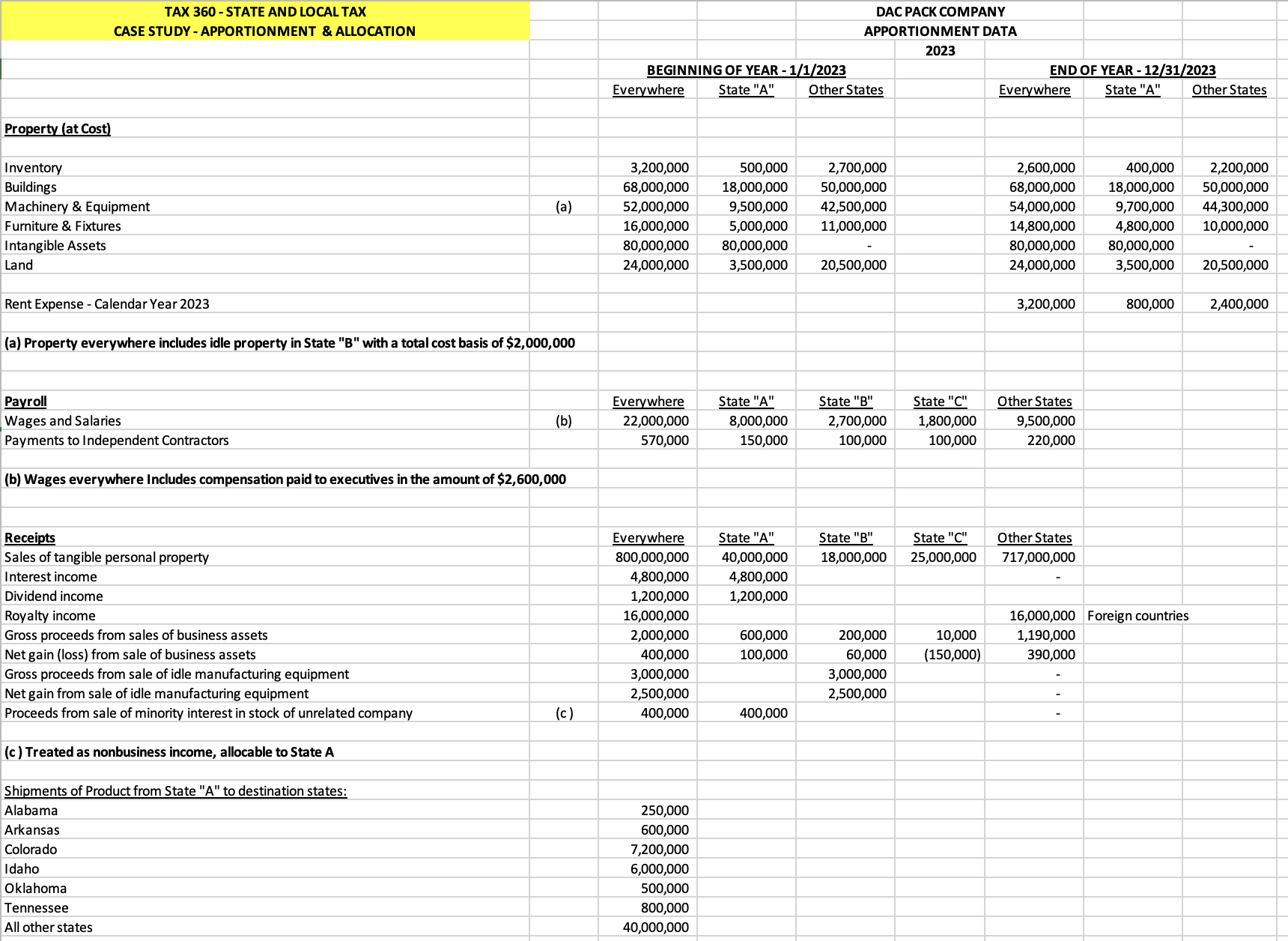

Case Studies - Apportionment & Allocation Please use the following facts and data from the attached worksheet to calculate DAC Pack Company's 3-factor apportionment percentage

Case Studies - Apportionment & Allocation

Please use the following facts and data from the attached worksheet to calculate DAC Pack Company's 3-factor apportionment percentage (double-weighted sales factor) for State "A." All the information provided relates to calendar year 2023.

Facts:

- DAC Pack is a leading global manufacturer of sports equipment and clothing, known mainly for its alpine skis and tennis racquets.

- DAC Pack's U.S. headquarters facility is located in State "A," a separate company reporting state. DAC Pack is incorporated in State "A." - property factor

- DAC Pack has manufacturing sites and distribution centers in State "A" and various other states.

- DAC Pack is subject to corporate income tax in every state except for Arkansas and Oklahoma.

- In addition to its employee complement, DAC Pack also uses independent contractors (non-employees) to assist with distribution center operations during peak periods. In 2023, DAC Pack spent $570,000 for the services of independent contractors.

- Compensation paid to Dac Pack's President, CEO, CFO, and Vice-Presidents totaled $2,600,000. All of the company's officers are based at Dac Pack's headquarters in State "A."

- On July 1, 2023, DAC Pack sold certain older manufacturing equipment in State "B" to a local company. This equipment had been idle for the past 3 years.The relevant information pertaining to this transaction:

- Cost basis of manufacturing equipment = $2,000,000 (at beginning of year). These assets are included in the apportionment data provided. - subtract from property

- Total proceeds from sale of equipment = $3,000,000.Net gain from sale of equipment = $2,500,000.

- DAC Pack received dividend income from its foreign (non-U.S.) subsidiaries. State "A" allows a 100% dividends received deduction for foreign dividends (i.e., this income is excluded from the tax base).

- DAC Pack received royalty income from its foreign (non-U.S.) subsidiaries for the use of manufacturing-related patents and know-how in their operations. These royalties were paid pursuant to licensing agreements.

- During 2023, DAC Pack sold its minority interest (10%) in the stock of an unrelated business that was being held as an investment.Proceeds from the stock sale were $400,000. DAC Pack will treat this as nonbusiness income for state income tax purposes, allocable to State "A."

Assumptions - State "A" general apportionment rules

- 3-factor apportionment method is used - property, payroll, and receipts (double-weighted receipts factor)

- Property owned is valued at original cost. The property values are averaged at the beginning and end of the year. Rented property is valued at 8 times the annual rent expense.

- Assets no longer used for business purposes - considered idle property and excluded from property factor after not being used for greater than 2 years

- Officers' compensation is excluded from the payroll factor

- Receipts factor:

- Interest is assigned to the state of commercial domicile

- Dividends are assigned to the state of commercial domicile

- Royalties are assigned to the location where the intangibles are used

- "Throwback" sales rule applies

- Sales of assets used in business - gross amount realized (gross proceeds), not net gain. Is reported for apportionment purposes

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting Tools For Business Decision Making

Authors: Jerry J. Weygandt, Paul D. Kimmel, Jill E. Mitchell

9th Edition

111970958X, 9781119709589