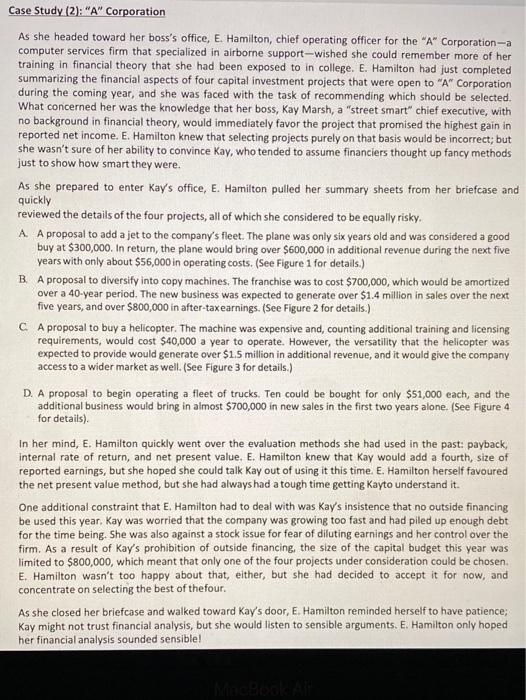

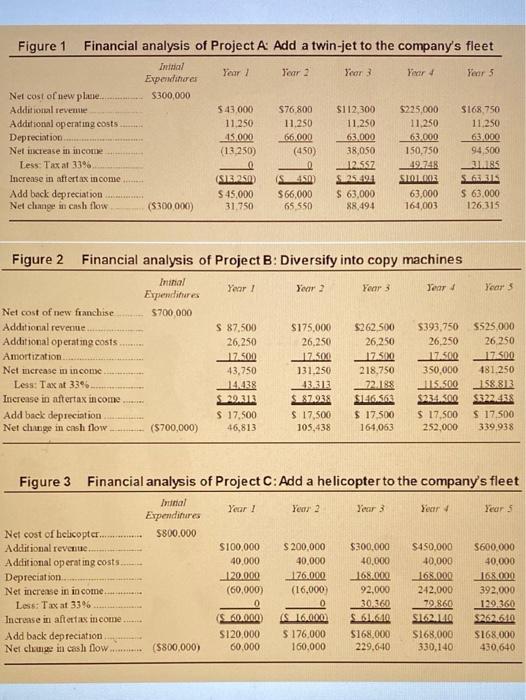

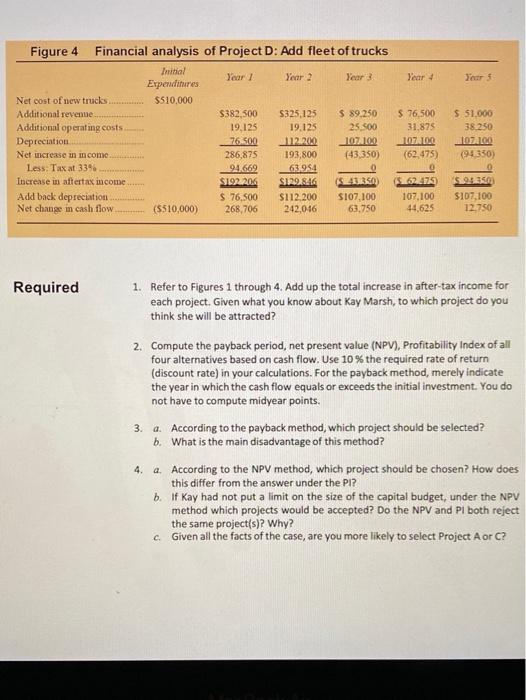

Case Study (2): "A" Corporation As she headed toward her boss's office, E. Hamilton, chief operating officer for the "A" Corporation-a computer services firm that specialized in airborne support-wished she could remember more of her training in financial theory that she had been exposed to in college. E. Hamilton had just completed summarizing the financial aspects of four capital investment projects that were open to "A" Corporation during the coming year, and she was faced with the task of recommending which should be selected. What concerned her was the knowledge that her boss, Kay Marsh, a "street smart" chief executive, with no background in financial theory, would immediately favor the project that promised the highest gain in reported net income. E. Hamilton knew that selecting projects purely on that basis would be incorrect, but she wasn't sure of her ability to convince Kay, who tended to assume financiers thought up fancy methods just to show how smart they were. As she prepared to enter Kay's office, E. Hamilton pulled her summary sheets from her briefcase and quickly reviewed the details of the four projects, all of which she considered to be equally risky. A. A proposal to add a jet to the company's fleet. The plane was only six years old and was considered a good buy at $300,000. In return, the plane would bring over $600,000 in additional revenue during the next five years with only about $56,000 in operating costs. (See Figure 1 for details.) B. A proposal to diversify into copy machines. The franchise was to cost $700,000, which would be amortized over a 40-year period. The new business was expected to generate over $1,4 million in sales over the next five years, and over $800,000 in after-taxearnings. (See Figure 2 for details.) C A proposal to buy a helicopter. The machine was expensive and counting additional training and licensing requirements, would cost $40,000 a year to operate. However, the versatility that the helicopter was expected to provide would generate over $1.5 million in additional revenue, and it would give the company access to a wider market as well. (See Figure 3 for details.) D. A proposal to begin operating a fleet of trucks. Ten could be bought for only $51,000 each, and the additional business would bring in almost $700,000 in new sales in the first two years alone. (See Figure 4 for details). In her mind, E. Hamilton quickly went over the evaluation methods she had used in the past: payback, internal rate of return, and net present value. E. Hamilton knew that Kay would add a fourth, size of reported earnings, but she hoped she could talk Kay out of using it this time. E. Hamilton herself favoured the net present value method, but she had always had a tough time getting Kayto understand it. One additional constraint that E. Hamilton had to deal with was Kay's insistence that no outside financing be used this year, Kay was worried that the company was growing too fast and had piled up enough debt for the time being. She was also against a stock issue for fear of diluting earnings and her control over the firm. As a result of Kay's prohibition of outside financing the size of the capital budget this year was limited to $800,000, which meant that only one of the four projects under consideration could be chosen. E. Hamilton wasn't too happy about that, either, but she had decided to accept it for now, and concentrate on selecting the best of the four. As she closed her briefcase and walked toward Kay's door, E. Hamilton reminded herself to have patience; Kay might not trust financial analysis, but she would listen to sensible arguments. E. Hamilton only hoped her financial analysis sounded sensible! Figure 1 Financial analysis of Project A Add a twin-jet to the company's fleet Inila Year / Experfahre Year 2 Your Yu 3 Year 5 Net cost of new place $300,000 Additional revente 543000 $76 800 $112.300 $225,000 $168.750 Additional operating costs 11.250 11.250 11.250 11.250 11.250 Depreciation 415.000 66.000 63.000 63.000 63.000 Net tease in income (13.250) (450) 38,050 150,750 94,500 Less: Tax at 33% 0 12.557 49.748 RS Increase in aftertax income (S2.25 ( SSM SA 25.401 SOLE 5.6335 Add back depreciation $ 45,000 $ 66,000 $ 63,000 63,000 $ 63,000 Net clunge in cash flow ($300.000) 31.750 65 550 88,494 164,003 126,315 Year 3 Figure 2 Financial analysis of Project B: Diversify into copy machines Ininal Year! Year Ferr3 Year Expenditures Net cost of new franchise 5700.000 Additional revenue S 87.500 $175,000 S262 500 $393.750 Additional operating costs 26,250 26.250 26,250 26.250 Amortization 117.500 17.500 LIZA 17.500 Net increase m income 43,750 131.250 218,750 350.000 Less: Tax at 33% 14.238 3312 72.188 15.500 Increase in aftertax income S2933 S87935 SE6550 $234.00 Add back depreciation $ 17.500 $ 17,500 $17.500 $ 17.500 Net change in cash flow ($700,000) 46,813 105,438 164.063 252,000 $525.000 26.250 17.500 181.250 158.8 $32714538 17.500 339.938 Figure 3 Financial analysis of Project C: Add a helicopter to the company's fleet Initial Year / Year 2 Year 3 Year Year 3 Expenditures Net cost of belicopter............ $800.000 Additional revenue S100.000 $ 200,000 $300.000 $450,000 $600.000 Additional operating costs. 40.000 40.000 40,000 40.000 40,000 Depreciation..... 120.000 176.000 168.00 168.000 168.000 Net increase in income. (60,000) (16,000 92.000 242.000 392,000 Less: Taxat 33% 0 30,360 79 860 129.360 Increase in after an income ($ 60.000) ( 16.00 5660 56210 $262640 Add back depreciation S120,000 $ 176,000 $168,000 S168,000 S168.000 Net che in cash flow ($800,000) 60.000 160.000 229,640 330,140 430,640 Yours Figure 4 Financial analysis of Project D: Add fleet of trucks Initial Year 1 Year 2 Year 3 Year Erpewiitures Net cost of new trucks $510,000 Additional revenue $382,500 $325,125 $ 89.250 $ 76,500 Additional operating costs 19.125 19.125 25 500 31.875 Depreciation 76.500 112200 LOZANO 107 Net wcrease in income 286,875 193,800 (43,350) (62.475) Less. Taxat 33% 94669 63954 Increase in aftertax income S192.206 S129.846 (S21350) (56275 Add back depreciation $ 76,500 S112 200 S107,100 107,100 Net change in cash flow (5510,000) 268,706 242,016 63.750 44.625 $ 51.000 38.250 107ALCO 94350) S.99.350 $107,100 12.750 Required 1. Refer to Figures 1 through 4. Add up the total increase in after-tax income for each project. Given what you know about Kay Marsh, to which project do you think she will be attracted? 2. Compute the payback period, net present value (NPV), Profitability Index of all four alternatives based on cash flow. Use 10% the required rate of return (discount rate) in your calculations. For the payback method, merely indicate the year in which the cash flow equals or exceeds the initial investment. You do not have to compute midyear points. 3. a. According to the payback method, which project should be selected? b. What is the main disadvantage of this method? 4. a. According to the NPV method, which project should be chosen? How does this differ from the answer under the Pl? b. If Kay had not put a limit on the size of the capital budget, under the NPV method which projects would be accepted? Do the NPV and Pl both reject the same project(s)? Why? c. Given all the facts of the case, are you more likely to select Project A or C