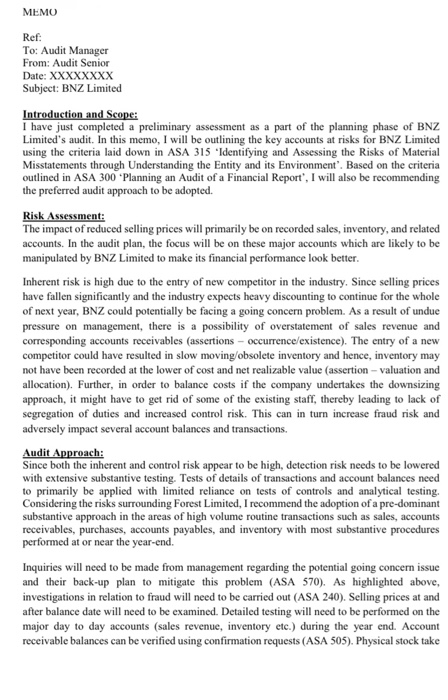

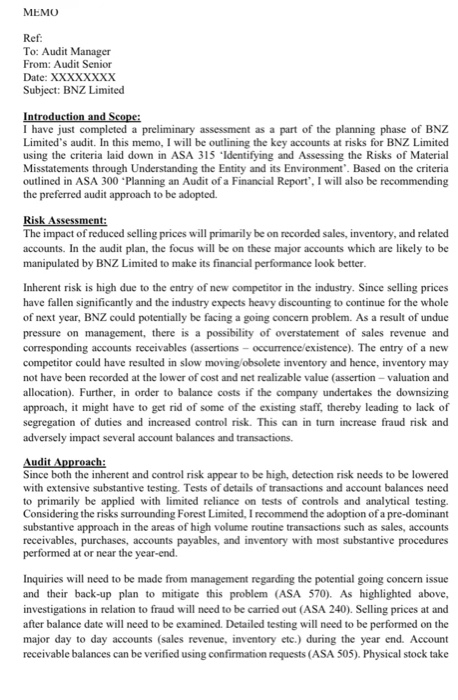

Case Study 2 - Auditing ACCT3000 (Semester 1.2020) You are an Audit Senior currently planning the 30 June 20x9 audits of Comp Limited (Comp), Health Limited (Health) and News Limited (News). At recently scheduled planning meetings with Comp, Health and News, you obtain the following overview of this year's operations for cach of the three client companies: Comp is a manufacturer of computer hardware. The old costing system that was developed in- house, could no longer keep up with the complex and detailed manufacturing costing process that provides tender/bid submission costings and the company's comprehensive reporting requirements. As a result, Comp purchased and installed a popular off the shelf (not customized) costing system to support the highly sophisticated and cost sensitive nature of its product designs. Since this system had been utilised by many other firms in the industry, Comp has not thoroughly tested the adequacy of the features and controls inherent within the system. At the same time, the staffs are not feeling confident with the new system due to lack of training and supervision. Staff are also concerned that data might be lost when converting to the new system. Health operates chemist shops in Perth. A large proportion of the sales transactions are conducted in cash. Health claims on having strong control policies and procedures in place to monitor the employees handling cash transactions and safeguarding the cash. However, the proper implementation of those policies had been questioned by the previous auditor. As Health is planning to expand to Mandurah and Busselton, it is applying for a bank loan to obtain additional funding for the expansion. Before approving the loan, the bank requires Health to provide them with an audited financial statement. The unaudited figures of current year suggest Health's revenue to have increased significantly by 25 percent from last year while the gross profit appears to have increased marginally by 5 percent. News has been in the paper manufacturing business for the last 17 years. It manufactures and distributes paper throughout the Australian continent. During the last five years, News opened four new factories in three different locations, financed mainly from bank loans. Due to rapid growth in the company, the financial director John Brown is keen to set up an internal audit department. Currently the project appears to have stalled, as some of the senior executives do not foresee the benefit of setting up such a department and are unwilling to commit any additional fund or resources on this plan. The senior executives argue that they are competent enough to monitor the internal controls of News. Required: Prepare a memorandum to the audit manager, outlining your risk assessments relating to Comp. Health and News. When making your risk assessments: (a) Identify and discuss the risks that may arise from each of the above companies. In your explanation, please mention the components of the audit risk model affected. (b) Identify how the audit plan will be affected and recommend specific audit procedures to address these risks. Assurance SK Assessment emester EXEMPLAR FOR CASE STUDY (Part 2) You are the Audit Senior currently planning the audit of BNZ Limited (BNZ), a manufacturing company. In the planning phase of the audit engagement you became aware that a new competitor of BNZ entered the market six months before year end and since that time selling prices have fallen significantly. Your inquiries have revealed that the industry expects heavy discounting to continue for the whole of next year. The Managing Director of BNZ told you that the company has already downsized some staff to balance costs. Required: Prepare a memorandum to the audit manager, outlining your risk assessment relating to BNZ Limited. When making your risk assessment: (a) Identify and discuss the risks that may arise from the information that you have gathered on BNZ. In your explanation, please mention the components of the audit risk model affected. (b) Identify how the audit plan will be affected and recommend specific audit procedures to address these risks. MEMO Ref: To: Audit Manager From: Audit Senior Date: XXXXXXXX Subject: BNZ Limited Introduction and Scope: I have just completed a preliminary assessment as a part of the planning phase of BNZ Limited's audit. In this memo, I will be outlining the key accounts at risks for BNZ Limited using the criteria laid down in ASA 315 "Identifying and Assessing the Risks of Material Misstatements through Understanding the Entity and its Environment". Based on the criteria outlined in ASA 300 Planning an Audit of a Financial Report', I will also be recommending the preferred audit approach to be adopted. Risk Assessment: The impact of reduced selling prices will primarily be on recorded sales, inventory, and related accounts. In the audit plan, the focus will be on these major accounts which are likely to be manipulated by BNZ Limited to make its financial performance look better. Inherent risk is high due to the entry of new competitor in the industry. Since selling prices have fallen significantly and the industry expects heavy discounting to continue for the whole of next year, BNZ could potentially be facing a going concern problem. As a result of undue pressure on management, there is a possibility of overstatement of sales revenue and corresponding accounts receivables (assertions- occurrence/existence). The entry of a new competitor could have resulted in slow moving/obsolete inventory and hence, inventory may not have been recorded at the lower of cost and net realizable value (assertion - valuation and allocation). Further, in order to balance costs if the company undertakes the downsizing approach, it might have to get rid of some of the existing staff, thereby leading to lack of segregation of duties and increased control risk. This can in turn increase fraud risk and adversely impact several account balances and transactions, Audit Approach: Since both the inherent and control risk appear to be high, detection risk needs to be lowered with extensive substantive testing. Tests of details of transactions and account balances need to primarily be applied with limited reliance on tests of controls and analytical testing. Considering the risks surrounding Forest Limited, I recommend the adoption of a pre-dominant substantive approach in the areas of high volume routine transactions such as sales, accounts receivables, purchases, accounts payables, and inventory with most substantive procedures performed at or near the year-end. Inquiries will need to be made from management regarding the potential going concern issue and their back-up plan to mitigate this problem (ASA 570). As highlighted above, investigations in relation to fraud will need to be carried out (ASA 240). Selling prices at and after balance date will need to be examined. Detailed testing will need to be performed on the major day to day accounts (sales revenue, inventory etc.) during the year end. Account receivable balances can be verified using confirmation requests (ASA 505). Physical stock take Case Study 2 - Auditing ACCT3000 (Semester 1, 2020) You are an Audit Senior currently planning the 30 June 20x9 audits of Comp Limited (Comp), Health Limited (Health) and News Limited (News). At recently scheduled planning meetings with Comp, Health and News, you obtain the following overview of this year's operations for cach of the three client companies: Comp is a manufacturer of computer hardware. The old costing system that was developed in- house, could no longer keep up with the complex and detailed manufacturing costing process that provides tender/bid submission costings and the company's comprehensive reporting requirements. As a result, Comp purchased and installed a popular off the shelf (not customized) costing system to support the highly sophisticated and cost sensitive nature of its product designs. Since this system had been utilised by many other firms in the industry, Comp has not thoroughly tested the adequacy of the features and controls inherent within the system. At the same time, the staffs are not feeling confident with the new system due to lack of training and supervision. Staff are also concemed that data might be lost when converting to the new system. Health operates chemist shops in Perth. A large proportion of the sales transactions are conducted in cash. Health claims on having strong control policies and procedures in place to monitor the employees handling cash transactions and safeguarding the cash. However, the proper implementation of those policies had been questioned by the previous auditor. As Health is planning to expand to Mandurah and Busselton, it is applying for a bank loan to obtain additional funding for the expansion. Before approving the loan, the bank requires Health to provide them with an audited financial statement. The unaudited figures of current year suggest Health's revenue to have increased significantly by 25 percent from last year while the gross profit appears to have increased marginally by 5 percent. News has been in the paper manufacturing business for the last 17 years. It manufactures and distributes paper throughout the Australian continent. During the last five years, News opened four new factories in three different locations, financed mainly from bank loans. Due to rapid growth in the company, the financial director John Brown is keen to set up an internal audit department. Currently the project appears to have stalled, as some of the senior executives do not foresee the benefit of setting up such a department and are unwilling to commit any additional fund or resources on this plan. The senior executives argue that they are competent enough to monitor the internal controls of News. Required: Prepare a memorandum to the audit manager, outlining your risk assessments relating to Comp. Health and News. When making your risk assessments: (a) Identify and discuss the risks that may arise from each of the above companies. In your explanation, please mention the components of the audit risk model affected. (6) Identify how the audit plan will be affected and recommend specific audit procedures to address these risks ACCT3000 Auditing, Assurance & Risk Assessment Semester 1, 2020 EXEMPLAR FOR CASE STUDY (Part 2) You are the Audit Senior currently planning the audit of BNZ Limited (BNZ), a manufacturing company. In the planning phase of the audit engagement you became aware that a new competitor of BNZ entered the market six months before year end and since that time selling prices have fallen significantly. Your inquiries have revealed that the industry expects heavy discounting to continue for the whole of next year. The Managing Director of BNZ told you that the company has already downsized some staff to balance costs. Required: Prepare a memorandum to the audit manager, outlining your risk assessment relating to BNZ Limited. When making your risk assessment: (a) Identify and discuss the risks that may arise from the information that you have gathered on BNZ. In your explanation, please mention the components of the audit risk model affected. (b) Identify how the audit plan will be affected and recommend specific audit procedures to address these risks. MEMO Ref: To: Audit Manager From: Audit Senior Date: XXXXXXXX Subject: BNZ Limited Introduction and Scope: I have just completed a preliminary assessment as a part of the planning phase of BNZ Limited's audit. In this memo, I will be outlining the key accounts at risks for BNZ Limited using the criteria laid down in ASA 315 "Identifying and Assessing the Risks of Material Misstatements through Understanding the Entity and its Environment'. Based on the criteria outlined in ASA 300 Planning an Audit of a Financial Report', I will also be recommending the preferred audit approach to be adopted. Risk Assessment: The impact of reduced selling prices will primarily be on recorded sales, inventory, and related accounts. In the audit plan, the focus will be on these major accounts which are likely to be manipulated by BNZ Limited to make its financial performance look better. Inherent risk is high due to the entry of new competitor in the industry. Since selling prices have fallen significantly and the industry expects heavy discounting to continue for the whole of next year, BNZ could potentially be facing a going concern problem. As a result of undue pressure on management, there is a possibility of overstatement of sales revenue and corresponding accounts receivables (assertions- occurrence/existence). The entry of a new competitor could have resulted in slow moving obsolete inventory and hence, inventory may not have been recorded at the lower of cost and net realizable value (assertion - valuation and allocation). Further, in order to balance costs if the company undertakes the downsizing approach, it might have to get rid of some of the existing staff, thereby leading to lack of segregation of duties and increased control risk. This can in turn increase fraud risk and adversely impact several account balances and transactions. Audit Approach: Since both the inherent and control risk appear to be high, detection risk needs to be lowered with extensive substantive testing. Tests of details of transactions and account balances need to primarily be applied with limited reliance on tests of controls and analytical testing. Considering the risks surrounding Forest Limited, I recommend the adoption of a pre-dominant substantive approach in the areas of high volume routine transactions such as sales, accounts receivables, purchases, accounts payables, and inventory with most substantive procedures performed at or near the year-end. Inquiries will need to be made from management regarding the potential going concern issue and their back-up plan to mitigate this problem (ASA 570). As highlighted above, investigations in relation to fraud will need to be carried out (ASA 240). Selling prices at and after balance date will need to be examined. Detailed testing will need to be performed on the major day to day accounts (sales revenue, inventory etc.) during the year end. Account receivable balances can be verified using confirmation requests (ASA 505). Physical stock take