Answered step by step

Verified Expert Solution

Question

1 Approved Answer

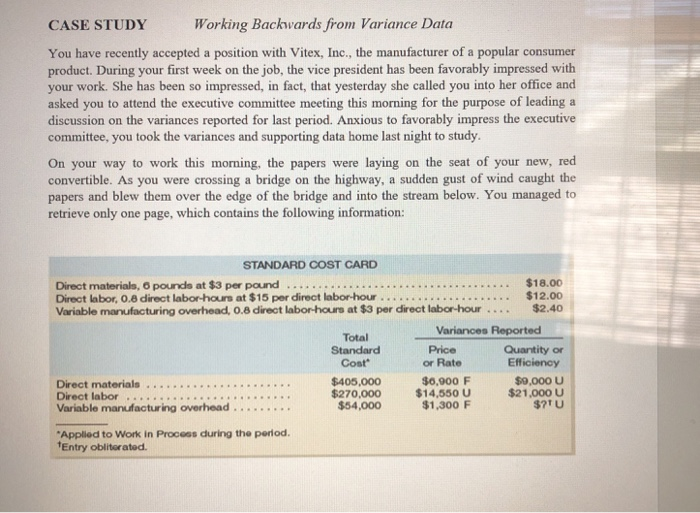

CASE STUDY Working Backwards from Variance Data You have recently accepted a position with Vitex, Inc., the manufacturer of a popular consumer product. During your

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stand Up To The IRS How To Handle Audits Tax Bills And Tax Court

Authors: Frederick W. Daily Robin Leonard

2nd Edition

0873372409, 978-0873372404