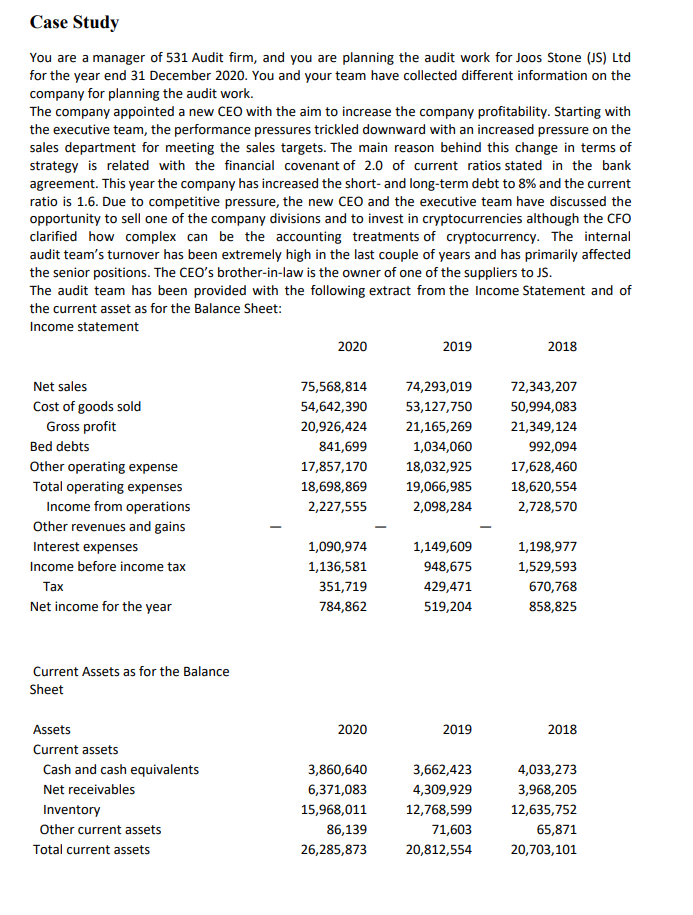

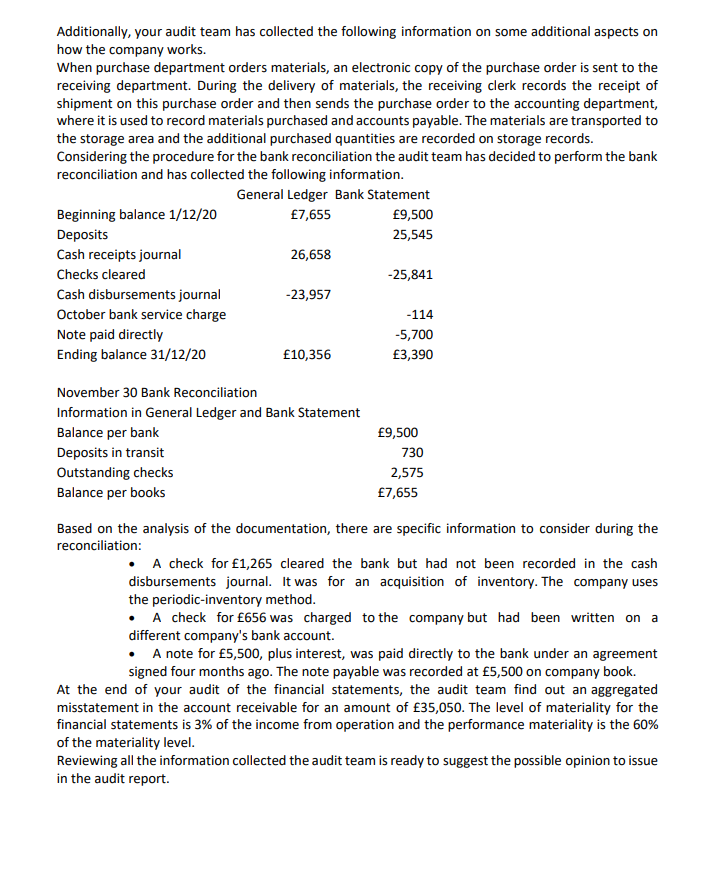

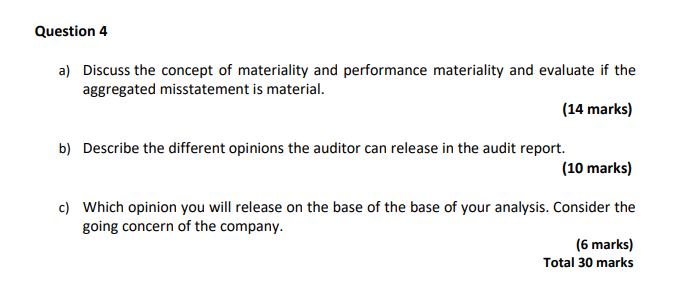

Case Study You are a manager of 531 Audit firm, and you are planning the audit work for Joos Stone (JS) Ltd for the year end 31 December 2020. You and your team have collected different information on the company for planning the audit work. The company appointed a new CEO with the aim to increase the company profitability. Starting with the executive team, the performance pressures trickled downward with an increased pressure on the sales department for meeting the sales targets. The main reason behind this change in terms of strategy is related with the financial covenant of 2.0 of current ratios stated in the bank agreement. This year the company has increased the short and long-term debt to 8% and the current ratio is 1.6. Due to competitive pressure, the new CEO and the executive team have discussed the opportunity to sell one of the company divisions and to invest in cryptocurrencies although the CFO clarified how complex can be the accounting treatments of cryptocurrency. The internal audit team's turnover has been extremely high in the last couple of years and has primarily affected the senior positions. The CEO's brother-in-law is the owner of one of the suppliers to JS. The audit team has been provided with the following extract from the Income Statement and of the current asset as for the Balance Sheet: Income statement 2020 2019 2018 Net sales Cost of goods sold Gross profit Bed debts Other operating expense Total operating expenses Income from operations Other revenues and gains Interest expenses Income before income tax Tax Net income for the year 75,568,814 54,642,390 20,926,424 841,699 17,857,170 18,698,869 2,227,555 74,293,019 53,127,750 21,165,269 1,034,060 18,032,925 19,066,985 2,098,284 72,343,207 50,994,083 21,349,124 992,094 17,628,460 18,620,554 2,728,570 1,090,974 1,136,581 351,719 784,862 1,149,609 948,675 429,471 519,204 1,198,977 1,529,593 670,768 858,825 Current Assets as for the Balance Sheet 2020 2019 2018 Assets Current assets Cash and cash equivalents Net receivables Inventory Other current assets Total current assets 3,860,640 6,371,083 15,968,011 86,139 26,285,873 3,662,423 4,309,929 12,768,599 71,603 20,812,554 4,033,273 3,968,205 12,635,752 65,871 20,703, 101 Additionally, your audit team has collected the following information on some additional aspects on how the company works. When purchase department orders materials, an electronic copy of the purchase order is sent to the receiving department. During the delivery of materials, the receiving clerk records the receipt of shipment on this purchase order and then sends the purchase order to the accounting department, where it is used to record materials purchased and accounts payable. The materials are transported to the storage area and the additional purchased quantities are recorded on storage records. Considering the procedure for the bank reconciliation the audit team has decided to perform the bank reconciliation and has collected the following information. General Ledger Bank Statement Beginning balance 1/12/20 7,655 9,500 Deposits 25,545 Cash receipts journal 26,658 Checks cleared -25,841 Cash disbursements journal -23,957 October bank service charge -114 Note paid directly -5,700 Ending balance 31/12/20 10,356 3,390 November 30 Bank Reconciliation Information in General Ledger and Bank Statement Balance per bank Deposits in transit Outstanding checks Balance per books 9,500 730 2,575 7,655 Based on the analysis of the documentation, there are specific information to consider during the reconciliation: A check for 1,265 cleared the bank but had not been recorded in the cash disbursements journal. It was for an acquisition of inventory. The company uses the periodic-inventory method. A check for 656 was charged to the company but had been written on a different company's bank account. A note for 5,500, plus interest, was paid directly to the bank under an agreement signed four months ago. The note payable was recorded at 5,500 on company book. At the end of your audit of the financial statements, the audit team find out an aggregated misstatement in the account receivable for an amount of 35,050. The level of materiality for the financial statements is 3% of the income from operation and the performance materiality is the 60% of the materiality level. Reviewing all the information collected the audit team is ready to suggest the possible opinion to issue in the audit report. Question 4 a) Discuss the concept of materiality and performance materiality and evaluate if the aggregated misstatement is material. (14 marks) b) Describe the different opinions the auditor can release in the audit report. (10 marks) c) Which opinion you will release on the base of the base of your analysis. Consider the going concern of the company. (6 marks) Total 30 marks Case Study You are a manager of 531 Audit firm, and you are planning the audit work for Joos Stone (JS) Ltd for the year end 31 December 2020. You and your team have collected different information on the company for planning the audit work. The company appointed a new CEO with the aim to increase the company profitability. Starting with the executive team, the performance pressures trickled downward with an increased pressure on the sales department for meeting the sales targets. The main reason behind this change in terms of strategy is related with the financial covenant of 2.0 of current ratios stated in the bank agreement. This year the company has increased the short and long-term debt to 8% and the current ratio is 1.6. Due to competitive pressure, the new CEO and the executive team have discussed the opportunity to sell one of the company divisions and to invest in cryptocurrencies although the CFO clarified how complex can be the accounting treatments of cryptocurrency. The internal audit team's turnover has been extremely high in the last couple of years and has primarily affected the senior positions. The CEO's brother-in-law is the owner of one of the suppliers to JS. The audit team has been provided with the following extract from the Income Statement and of the current asset as for the Balance Sheet: Income statement 2020 2019 2018 Net sales Cost of goods sold Gross profit Bed debts Other operating expense Total operating expenses Income from operations Other revenues and gains Interest expenses Income before income tax Tax Net income for the year 75,568,814 54,642,390 20,926,424 841,699 17,857,170 18,698,869 2,227,555 74,293,019 53,127,750 21,165,269 1,034,060 18,032,925 19,066,985 2,098,284 72,343,207 50,994,083 21,349,124 992,094 17,628,460 18,620,554 2,728,570 1,090,974 1,136,581 351,719 784,862 1,149,609 948,675 429,471 519,204 1,198,977 1,529,593 670,768 858,825 Current Assets as for the Balance Sheet 2020 2019 2018 Assets Current assets Cash and cash equivalents Net receivables Inventory Other current assets Total current assets 3,860,640 6,371,083 15,968,011 86,139 26,285,873 3,662,423 4,309,929 12,768,599 71,603 20,812,554 4,033,273 3,968,205 12,635,752 65,871 20,703, 101 Additionally, your audit team has collected the following information on some additional aspects on how the company works. When purchase department orders materials, an electronic copy of the purchase order is sent to the receiving department. During the delivery of materials, the receiving clerk records the receipt of shipment on this purchase order and then sends the purchase order to the accounting department, where it is used to record materials purchased and accounts payable. The materials are transported to the storage area and the additional purchased quantities are recorded on storage records. Considering the procedure for the bank reconciliation the audit team has decided to perform the bank reconciliation and has collected the following information. General Ledger Bank Statement Beginning balance 1/12/20 7,655 9,500 Deposits 25,545 Cash receipts journal 26,658 Checks cleared -25,841 Cash disbursements journal -23,957 October bank service charge -114 Note paid directly -5,700 Ending balance 31/12/20 10,356 3,390 November 30 Bank Reconciliation Information in General Ledger and Bank Statement Balance per bank Deposits in transit Outstanding checks Balance per books 9,500 730 2,575 7,655 Based on the analysis of the documentation, there are specific information to consider during the reconciliation: A check for 1,265 cleared the bank but had not been recorded in the cash disbursements journal. It was for an acquisition of inventory. The company uses the periodic-inventory method. A check for 656 was charged to the company but had been written on a different company's bank account. A note for 5,500, plus interest, was paid directly to the bank under an agreement signed four months ago. The note payable was recorded at 5,500 on company book. At the end of your audit of the financial statements, the audit team find out an aggregated misstatement in the account receivable for an amount of 35,050. The level of materiality for the financial statements is 3% of the income from operation and the performance materiality is the 60% of the materiality level. Reviewing all the information collected the audit team is ready to suggest the possible opinion to issue in the audit report. Question 4 a) Discuss the concept of materiality and performance materiality and evaluate if the aggregated misstatement is material. (14 marks) b) Describe the different opinions the auditor can release in the audit report. (10 marks) c) Which opinion you will release on the base of the base of your analysis. Consider the going concern of the company. (6 marks) Total 30 marks