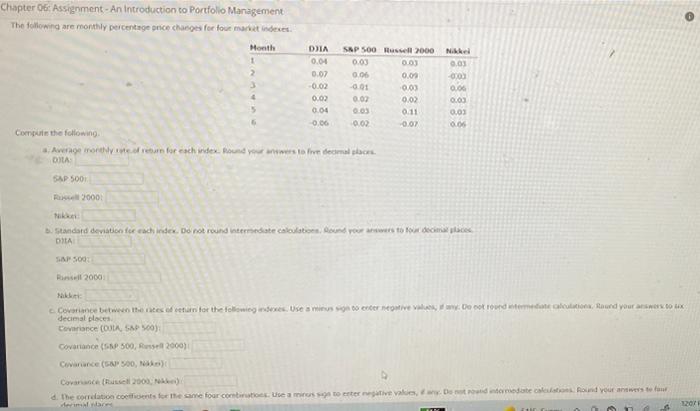

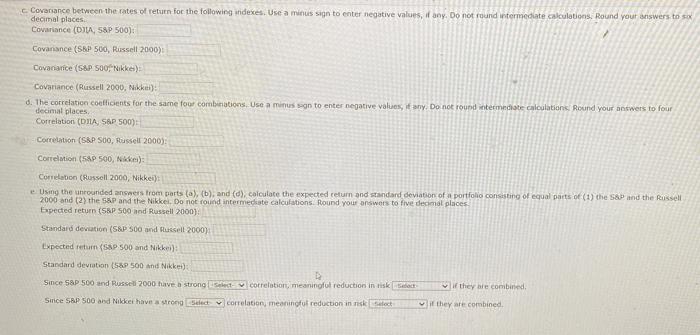

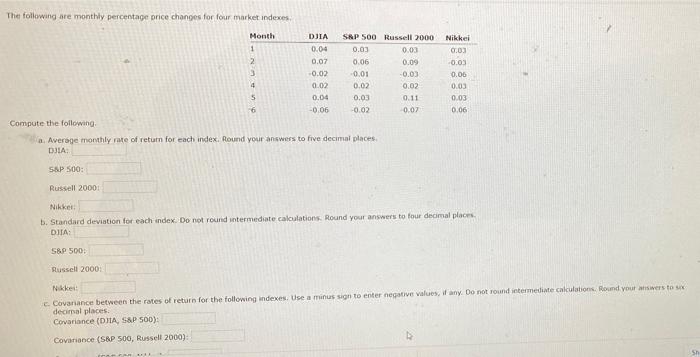

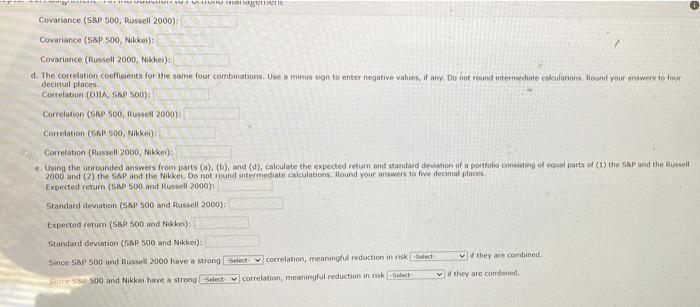

Chapter 06: Assignment - An Introduction to Portfolio Management The following are monthly percentage price changes for four market indexes. DIA Month SAP 500 Russell 2000 1 0.04 0.03 0.03 0.07 0.00 0.00 3 0.02 -0.01 0.03 0.00 0.02 0.02 0.04 DID 0.11 0.00 0.02 0.02 Compute the following Awe try to return for each wdex. Round you to decimal DILA Nikkel 0.03 -0.00 0.06 OLOS 0.03 0.06 SAP 5001 2000 Nike Standard deviation for each index. Do not round Intermediate calculation your worstof decimales DIA SAP 500 Ruswil 2009 Nak Covariance between the rate of earn for the following users to creative Decoroorden Round your answer. LX decimal places Covariance (DUA, SAPO) Covariance (P 500, Russell 2000) Cuvanance (A500) Covances 2000 d. the correlation coeficients for the same for como Use a mis to enter tive value www.domedate le Round your answers to deri 1207 Covariance between the rates of return for the following indexes. Use a minus sign to enter negative values, if any. Do not found intermediate calculations. Round your answers to sex decimal places Covariance (D, 58P 500) Covariance (S&P 500, Russell 2000) Covariatice (58P SOONikkers) Covariance (Russell 2000, Nikki) d. The correlation coefficients for the same for combinations. Use a minus son to enter negative values, if any. Do not found intermediate calculation Round your answers to four decimal places Correlation (DUA, SAP 500) Correlation (S&P 500, Russell 2000): Correlation (S&P 500, Nike Correlaton (Russell 2000, Nikkei) Using the unrounded answers from parts (a), (b), and (d), calculate the expected return and standard deviation of a portfolio consisting of equal parts of (1) the S&P and the Russell 2000 and (2) the S&P and the Nikkel. Do not found intermediate calculations. Round your answers to five decimal places Expected return (S&P 500 and Russell 2000) Standard deviation (S&P 500 and Russell 2000) Expected return (S&P 500 and Nikkei) Standard deviation (5&P 500 and Nikket) Since S&P 500 and Russell 2000 have strong correlation, meaningful reduction in risk if they are combined Sinice SP 500 and Nilket have a strong Liect correlation meaningful reduction in iskalect if they are combined DIA The following are monthly percentage price changes for four market indexes Month SAP 500 Russell 2000 1 0.04 0.03 0.03 2 0.07 0.06 0.09 3 -0.02 -0.01 -0.03 4 0.02 0.02 0.02 5 0.04 0.03 0.11 6 -0.06 -0.02 0.07 Compute the following a. Average monthly rate of return for each index. Round your answers to five decimal places DIA Nikkei 0.03 -0.03 0.06 0.03 0.03 0.06 5&P 500: Russell 2000: Nikker b. Standard deviation for each index. Do not round Intermediate calculations. Round your answers to four decimal places DIA: S&P 500 Russell 2000 Nikker: c. Covariance between the rates of return for the following indexes. Use a minus sign to enter negative values, if any. Do not found intermediate calculations. Round your answers to sex decimal places Covariance (DIA, S&P 500): Covariance (S&P 500, Russell 2000) UUSIMIN Covariance (SAP 500, Russell 2000): Covenance (58P 500, Nikkel): Covariance (Russell 2000, Nikker: d. The correlation coefficients for the same four combinations. Use a minus sign to enter negative values, if any. Do not found intermediate calculations. Round your answers to our decimal places Correlation (DJIA, SAP 500) Correlation (SAP 500, Russell 2000) Correlation (AP 500, Nikki) Correlation (Russell 2000, Nikkel): Using the unrounded answers from parts (a), (b), and (d), calculate the expected return and standard deviation of a portfolio consisting of parts of (1) the SAP and the Russell 2000 and (2) the S&P and the Nikkel. Do not found intermediate calculations, Round your answers to live decimal places Expected return (SAP 500 and Russell 2000) Standard deviation (S&P 500 and Russell 2000) Expected return (S&P 500 und Nikkei); Standard deviation (S&P 500 and Nikkel): Since S&P 500 and Russell 2000 have a strong Select correlation, meaningful reduction in risk Select they are combined. SR 500 and Nikkel have a strong Select correlation, meaningful reduction in risk Select if they are combined