Answered step by step

Verified Expert Solution

Question

1 Approved Answer

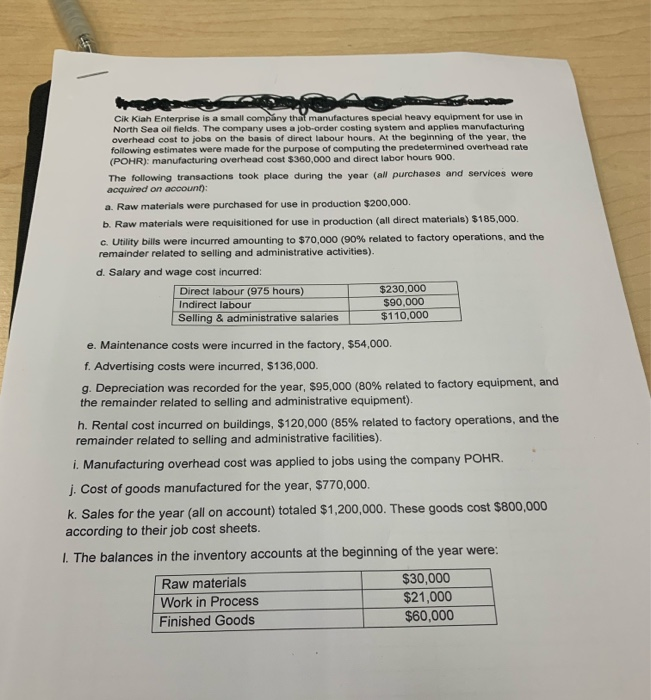

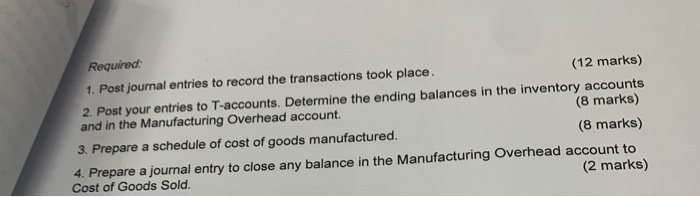

Cik Kiah Enterprise is a small company that manufactures special heavy equipment for use in North Sea oil fields. The company uses a job-order costing

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Carl L. Moore

5th Edition

0538019409, 978-0538019408