Answered step by step

Verified Expert Solution

Question

1 Approved Answer

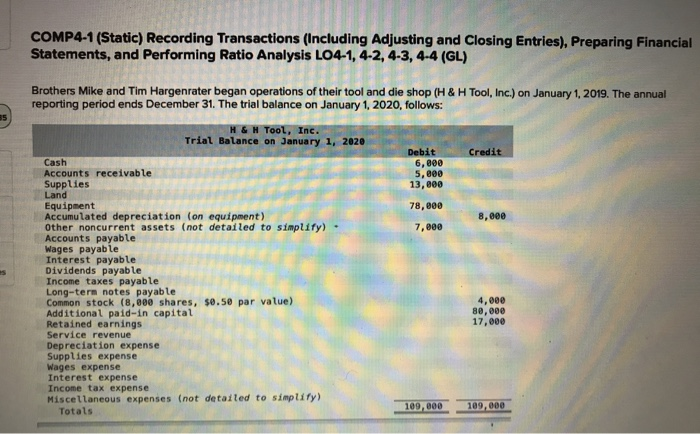

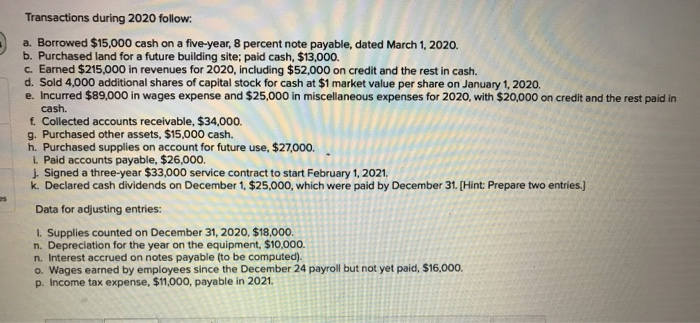

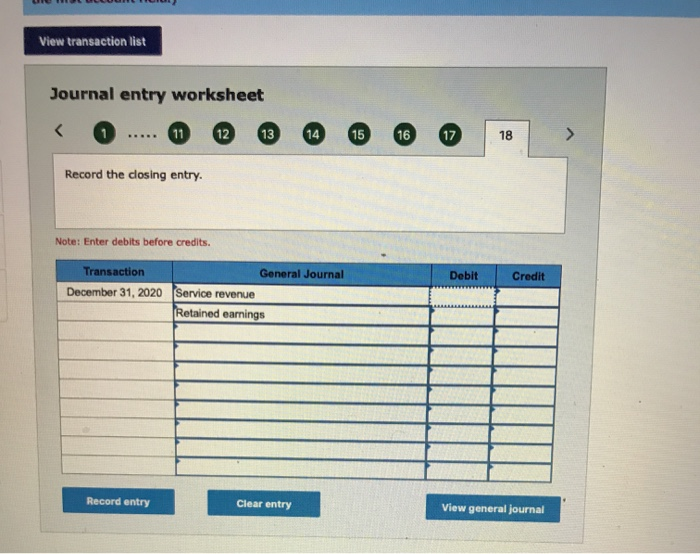

COMP4-1 (Static) Recording Transactions (Including Adjusting and Closing Entries), Preparing Financial Statements, and Performing Ratio Analysis L04-1, 4-2, 4-3, 4-4 (GL) 55 Brothers Mike and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Guidelines For Auditing Process Safety Management Systems

Authors: CCPS Center For Chemical Process Safety

2nd Edition

0470282355, 978-0470282359