Answered step by step

Verified Expert Solution

Question

1 Approved Answer

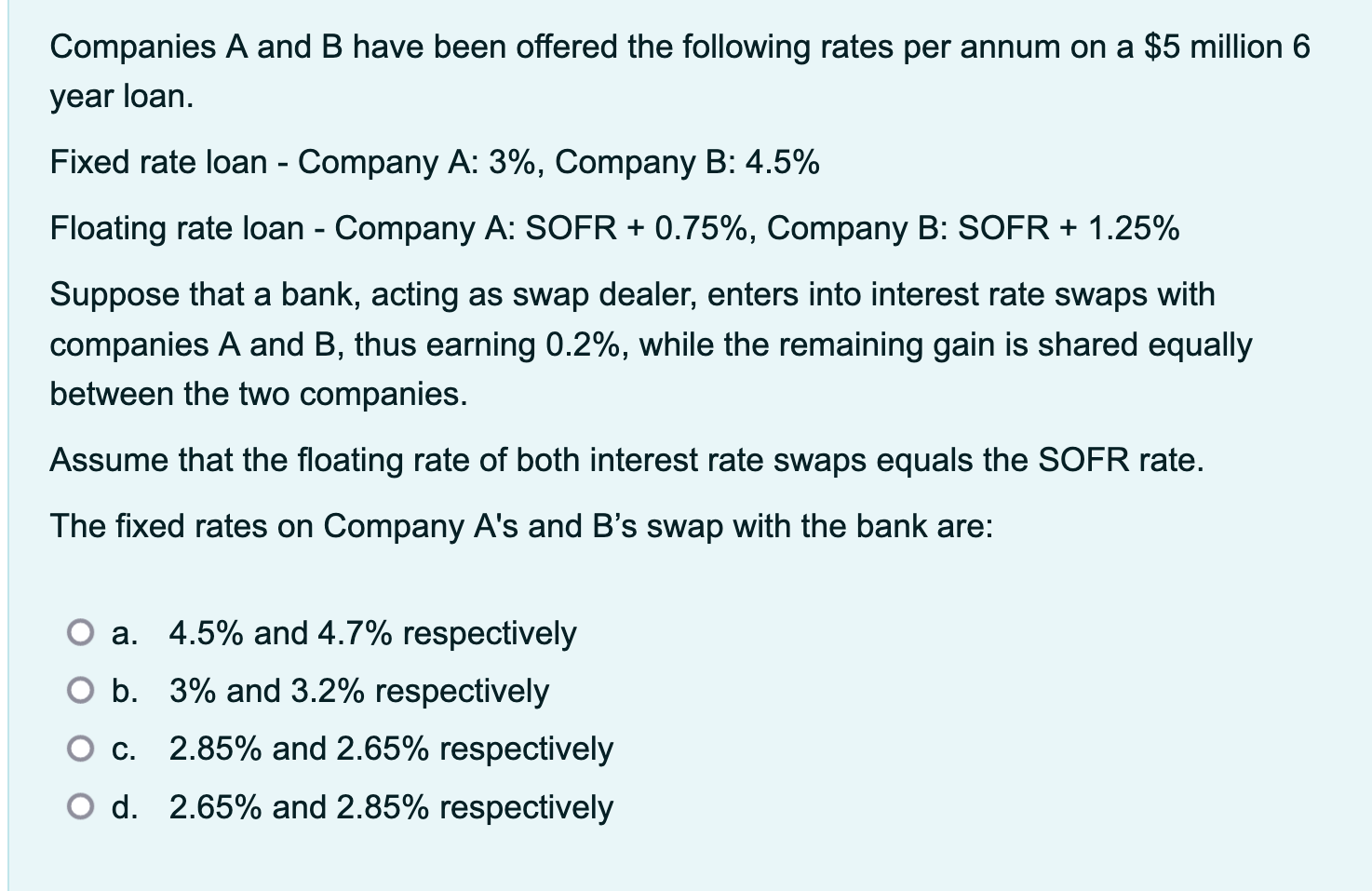

Companies A and B have been offered the following rates per annum on a $5 million 6 year loan. Fixed rate loan - Company

Companies A and B have been offered the following rates per annum on a $5 million 6 year loan. Fixed rate loan - Company A: 3%, Company B: 4.5% Floating rate loan - Company A: SOFR + 0.75%, Company B: SOFR + 1.25% Suppose that a bank, acting as swap dealer, enters into interest rate swaps with companies A and B, thus earning 0.2%, while the remaining gain is shared equally between the two companies. Assume that the floating rate of both interest rate swaps equals the SOFR rate. The fixed rates on Company A's and B's swap with the bank are: a. 4.5% and 4.7% respectively O b. 3% and 3.2% respectively C. 2.85% and 2.65% respectively O d. 2.65% and 2.85% respectively

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Analysis for Management

Authors: Barry Render, Ralph M. Stair, Michael E. Hanna, Trevor S. Ha

12th edition

133507335, 978-0133507331