Question

Company ABC is a seller of Oil, for which all sales take place at the end of the year. They wish to stabilize their earnings

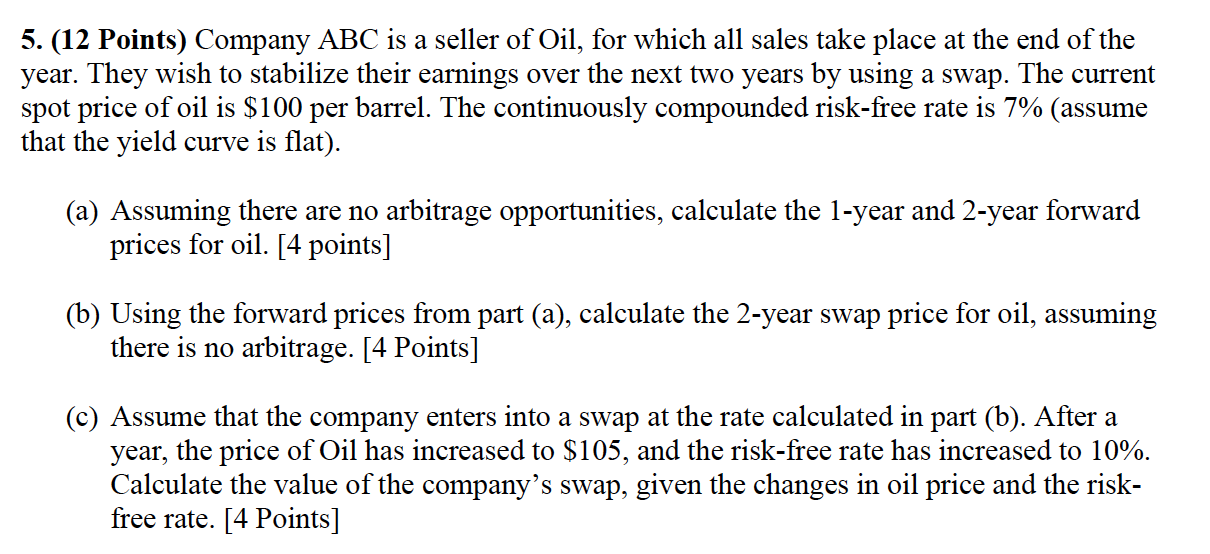

Company ABC is a seller of Oil, for which all sales take place at the end of the

year. They wish to stabilize their earnings over the next two years by using a swap. The current

spot price of oil is $100 per barrel. The continuously compounded risk-free rate is 7% (assume

that the yield curve is flat).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Theory Practice And Techniques In Bookkeeping Accounting And Auditing

Authors: N/A,

1st Edition

1680947761, 978-1680947762