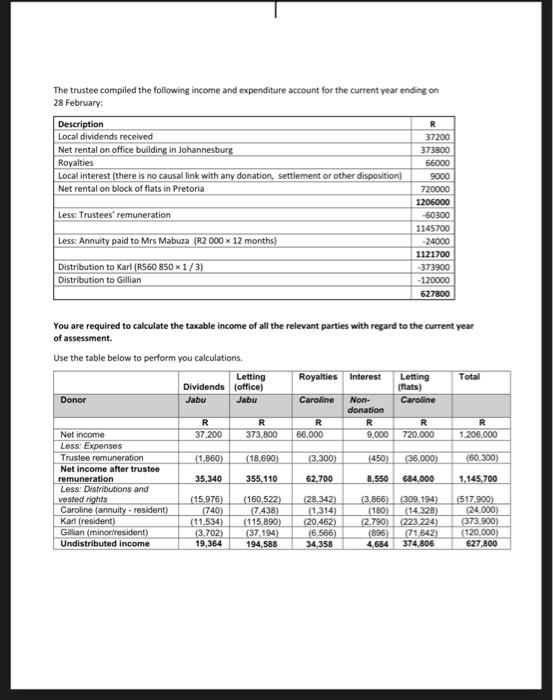

Comprehensive example During his lifetime, Jabu Mabuza created a trust for the benefit of the following beneficiaries: - his son, Karl Mabuza, who is 25 years old and lives in the Republic; - his unmarried daughter, Gillian Mabuza, who is 15 years old and lives in the Republic; and - his mother, Mrs. Caroline Mabuza ( 60 years old), who is a widow and lives in the Republic. Jabu Mabuza also lives in South Africa and donated the following assets to the trust: - shares in South African companies; and - the use of a large office bullding in Johannesburg for a period of ten years. At the end of the ten-year period, Mr. Mabuza will regain the full right of ownership of the property. The office building was erected before 2007. Mrs. Caroline Mabuza, 60 years old and grandmother of the children, also donated certain assets to the trust: - a block of flats in Pretoria that she inherited from her deceased husband; and - a patent that her deceased husband developed that is used by a manufacturing company in the Republic. The following clauses, among others, appear in the trust deed: (i) An annuity of R2, 000 per month is payable to Mrs. Caroline Mabuza for the rest of her life. (ii) After deduction of the trustee remuneration and the annuity to Mrs. Caroline Mabuza, one-third of the net income of the trust is payable to KarL. (iii) The trustee may distribute as much of the remaining third to Gillian for her education as is necessary y according g to his discretion. The rest of the income must be left in the trust until Gillian turns 25 , when the balance must be paid out to her and she must share in the income with her brothers on an equal basis. If Gillian should die before the age of 25 , the unpaid balance will be distributed to her brothers. (iv) Mr. Mabuza reserved the right to transfer Gillian's right to her share of the trust income in equal parts to her brothers if she were to marry before the age of 25 years. (v) The trustees' remuneration amounts to 5% of the net income of the trust, before the deduction of any distributions to the beneficiaries. The trustees are all independent third parties. (vi) All distributions of income are paid proportionately from all sources of income. (vii) All income received by the trust was received from a source within the Republic. The trustee compiled the following income and expenditure account for the current year ending on 28 February: You are required to calculate the taxable income of all the relevant parties with regard to the current year of assessment. Use the table below to perform you calculations