Answered step by step

Verified Expert Solution

Question

1 Approved Answer

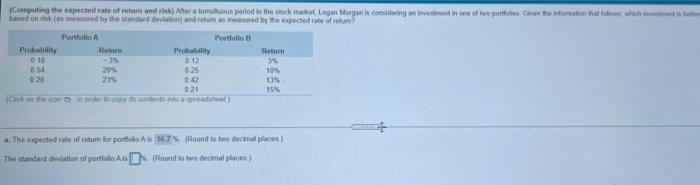

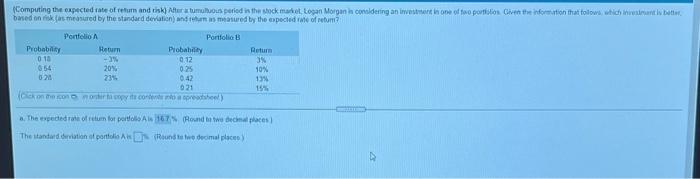

Computing the expected to return antik Anete tumutoon period in the stock market Logan Morgan in coming an investment in one of two parto Civetta

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The China Model Experience And Challenges

Authors: Yongnian Zheng

1st Edition

1433172003, 1433190214, 9781433190216