Question

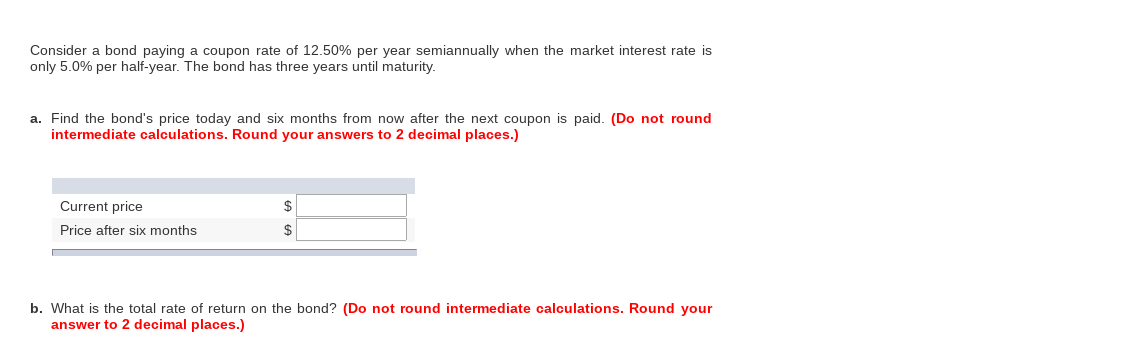

Consider a bond paying a coupon rate of 12.50% per year semiannually when the market interest rate is only 5.0% per half-year. The bond has

| Consider a bond paying a coupon rate of 12.50% per year semiannually when the market interest rate is only 5.0% per half-year. The bond has three years until maturity. |

| a. | Find the bond's price today and six months from now after the next coupon is paid. (Do not round intermediate calculations. Round your answers to 2 decimal places.) |

| Current price | $ |

| Price after six months | $ |

| b. | What is the total rate of return on the bond? (Do not round intermediate calculations. Round your answer to 2 decimal places.) |

| Total rate of return | % per six months |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Deregulation A Historical Perspective

Authors: Alexis Drach, Youssef Cassis

1st Edition

978-0198856955