Answered step by step

Verified Expert Solution

Question

1 Approved Answer

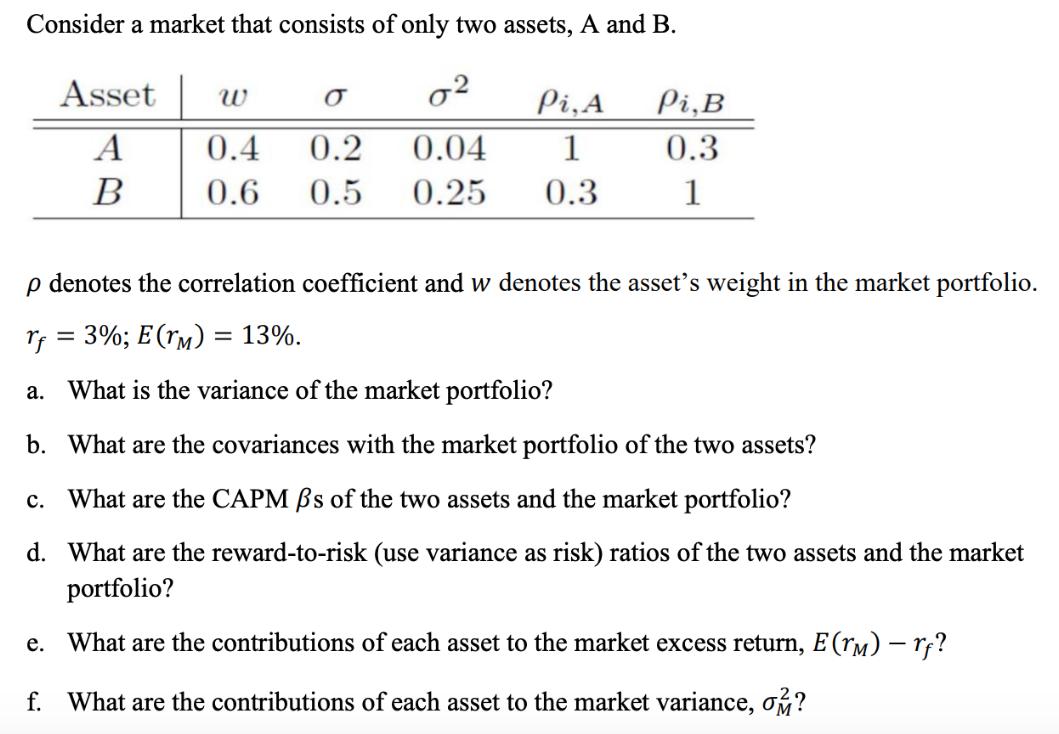

Consider a market that consists of only two assets, A and B. 0 0.04 0.25 Asset W A B 0.4 0.2 0.6 0.5 Pi,

Consider a market that consists of only two assets, A and B. 0 0.04 0.25 Asset W A B 0.4 0.2 0.6 0.5 Pi, A 1 0.3 = 13%. Pi, B 0.3 1 p denotes the correlation coefficient and w denotes the asset's weight in the market portfolio. rf = 3%; E(M) a. What is the variance of the market portfolio? b. What are the covariances with the market portfolio of the two assets? c. What are the CAPM s of the two assets and the market portfolio? d. What are the reward-to-risk (use variance as risk) ratios of the two assets and the market portfolio? e. What are the contributions of each asset to the market excess return, E(rm) - rf? f. What are the contributions of each asset to the market variance, o?

Step by Step Solution

★★★★★

3.51 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

The provided image contains a problem statement and a table showing information about two assets A and B which are the only assets in a market The problem is broken down into six parts each asking for ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Basic Statistics

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021