Question

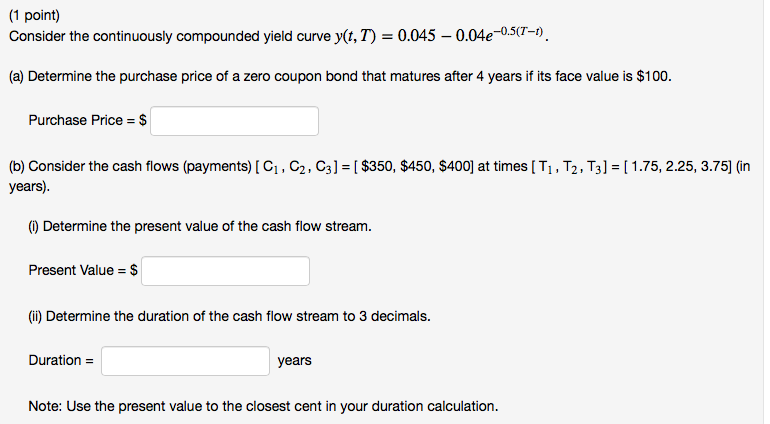

Consider the continuously compounded yield curve y(t,T)=0.045-0.04e^(-0.5)(T-t) (a) Determine the purchase price of a zero coupon bond that matures after 4 years if its face

Consider the continuously compounded yield curve y(t,T)=0.045-0.04e^(-0.5)(T-t)

(a) Determine the purchase price of a zero coupon bond that matures after 4 years if its face value is $100.

(b) Consider the cash flows (payments) [ C1, C2, C3] = [ $350, $450, $400] at times [ T1, T2, T3] = [ 1.75, 2.25, 3.75] (in years).

(i) Determine the present value of the cash flow stream.

(ii) Determine the duration of the cash flow stream to 3 decimals

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fraud examination

Authors: Steve Albrecht, Chad Albrecht, Conan Albrecht, Mark zimbelma

4th edition

538470844, 978-0538470841