Answered step by step

Verified Expert Solution

Question

1 Approved Answer

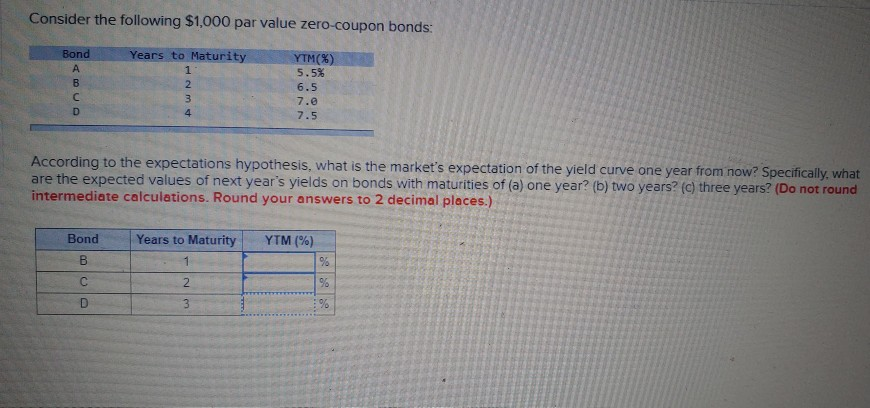

Consider the following $1,000 par value zero-coupon bonds: Bond B C D Years to Maturity 1 2 3 4 YTM(%) 5.5% 6.5 7.0 7.5 According

Consider the following $1,000 par value zero-coupon bonds: Bond B C D Years to Maturity 1 2 3 4 YTM(%) 5.5% 6.5 7.0 7.5 According to the expectations hypothesis, what is the market's expectation of the yield curve one year from now? Specifically, what are the expected values of next year's yields on bonds with maturities of (a) one year? (b) two years? (c) three years? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Bond Years to Maturity YTM (%) B % C 2 % D 3 %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: Philip J. Adelman; Alan M. Marks

6th edition

9780133099096, 133140512, 133099091, 978-0133140514