Answered step by step

Verified Expert Solution

Question

1 Approved Answer

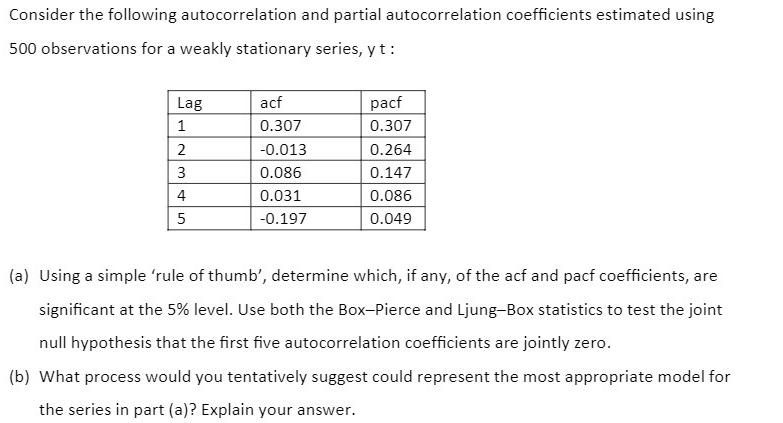

Consider the following autocorrelation and partial autocorrelation coefficients estimated using 500 observations for a weakly stationary series, yt: Lag 1 2 34 4 5

Consider the following autocorrelation and partial autocorrelation coefficients estimated using 500 observations for a weakly stationary series, yt: Lag 1 2 34 4 5 acf 0.307 -0.013 0.086 0.031 -0.197 pacf 0.307 0.264 0.147 0.086 0.049 (a) Using a simple 'rule of thumb', determine which, if any, of the acf and pacf coefficients, are significant at the 5% level. Use both the Box-Pierce and Ljung-Box statistics to test the joint null hypothesis that the first five autocorrelation coefficients are jointly zero. (b) What process would you tentatively suggest could represent the most appropriate model for the series in part (a)? Explain your answer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

SOLUTION a Using a simple rule of thumb to determine significance at the 5 level we look for coefficients that exceed the bounds of the confidence int...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Business Decision Making And Analysis

Authors: Robert Stine, Dean Foster

2nd Edition

978-0321836519, 321836510, 978-0321890269