Answered step by step

Verified Expert Solution

Question

1 Approved Answer

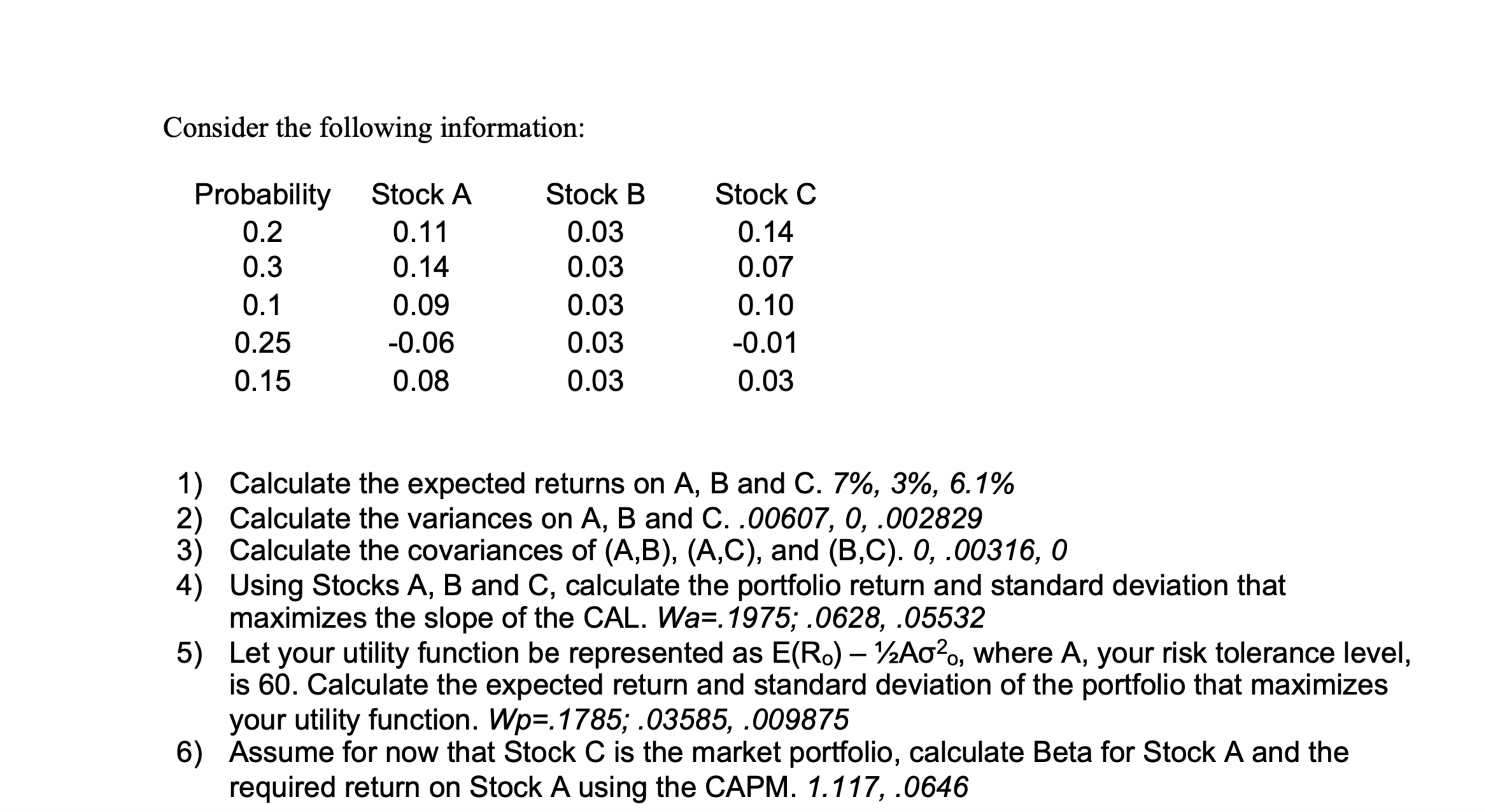

Consider the following information: Calculate the expected returns on A , B and C . 7 % , 3 % , 6 . 1 %

Consider the following information:

Calculate the expected returns on and C

Calculate the variances on A B and C

Calculate the covariances of ABAC and BC O

Using Stocks A B and C calculate the portfolio return and standard deviation that

maximizes the slope of the CAL. ;

Let your utility function be represented as where your risk tolerance level,

is Calculate the expected return and standard deviation of the portfolio that maximizes

your utility function. ;

Assume for now that Stock C is the market portfolio, calculate Beta for Stock A and the

required return on Stock A using the CAPM.

Please build through excel using excel formulas

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bankers Handbook On Credit Management

Authors: Indian Institute Of Banking & Finance

1st Edition

9387957853, 978-9387957855