Answered step by step

Verified Expert Solution

Question

1 Approved Answer

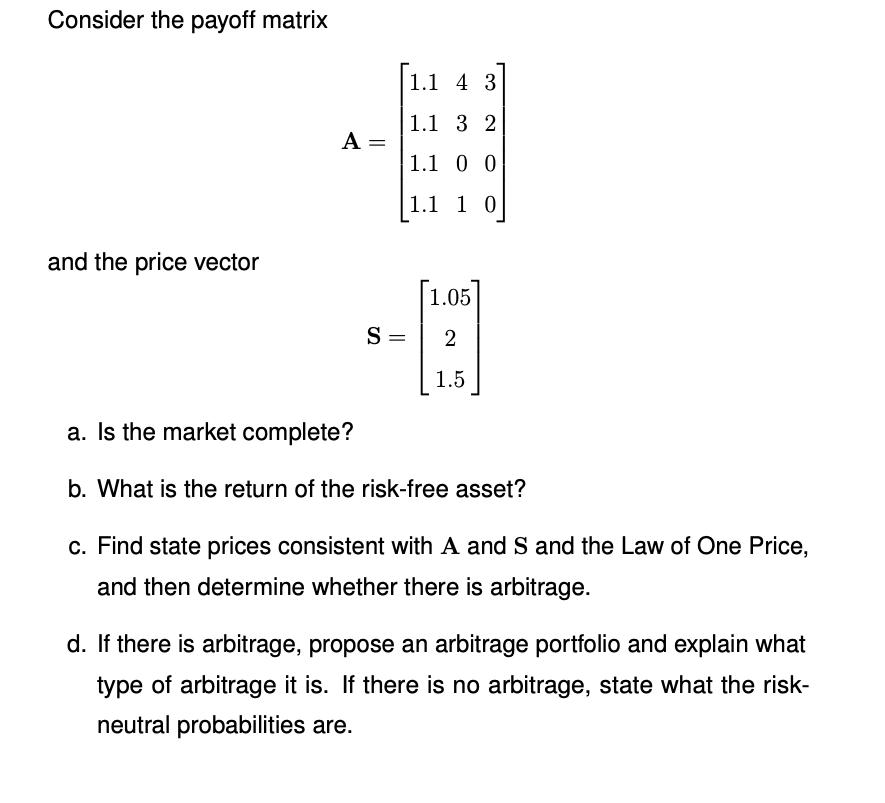

Consider the payoff matrix and the price vector A = S= = 1.1 4 3 1.1 3 2 1.1 0 0 1.1 1 0

Consider the payoff matrix and the price vector A = S= = 1.1 4 3 1.1 3 2 1.1 0 0 1.1 1 0 [1.05 2 1.5 a. Is the market complete? b. What is the return of the risk-free asset? c. Find state prices consistent with A and S and the Law of One Price, and then determine whether there is arbitrage. d. If there is arbitrage, propose an arbitrage portfolio and explain what type of arbitrage it is. If there is no arbitrage, state what the risk- neutral probabilities are.

Step by Step Solution

★★★★★

3.45 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516