Answered step by step

Verified Expert Solution

Question

1 Approved Answer

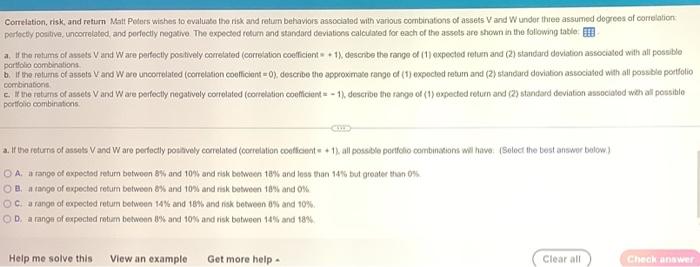

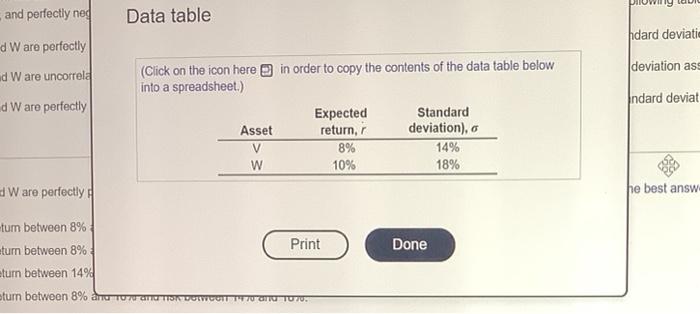

Correlation, risk, and return Matt Peters wishes to evaluate the risk and return bahaviors associated with various combinations of assets and under the assumed dogrees

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Unretirement How Baby Boomers Are Changing The Way We Think About Work Community And The Good Life

Authors: Chris Farrell

1st Edition

1632863235,1620401584