Answered step by step

Verified Expert Solution

Question

1 Approved Answer

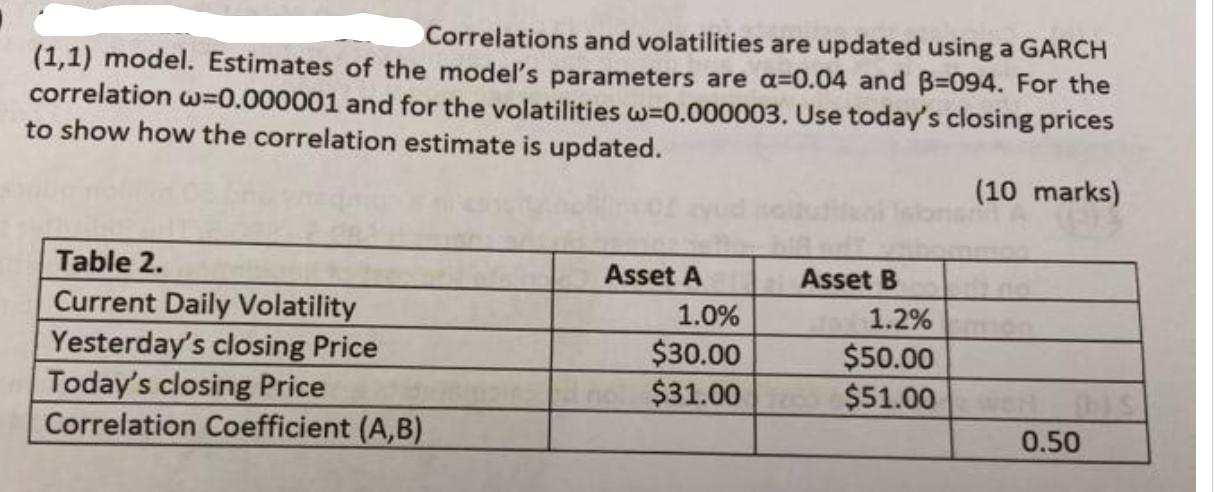

Correlations and volatilities are updated using a GARCH (1,1) model. Estimates of the model's parameters are a=0.04 and B=094. For the correlation w=0.000001 and

Correlations and volatilities are updated using a GARCH (1,1) model. Estimates of the model's parameters are a=0.04 and B=094. For the correlation w=0.000001 and for the volatilities w=0.000003. Use today's closing prices to show how the correlation estimate is updated. Table 2. Current Daily Volatility Yesterday's closing Price Today's closing Price Correlation Coefficient (A,B) Asset A 1.0% $30.00 $31.00 Asset B 1.2% $50.00 $51.00 (10 marks) TA (2) wer this 0.50

Step by Step Solution

★★★★★

3.38 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

To update the correlation estimate using the GARCH 11 model we can use the follow...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures and Other Derivatives

Authors: John C. Hull

10th edition

013447208X, 978-0134472089