Could you please breakdown the cash-inflow/outflow and reasons for. Thank you!

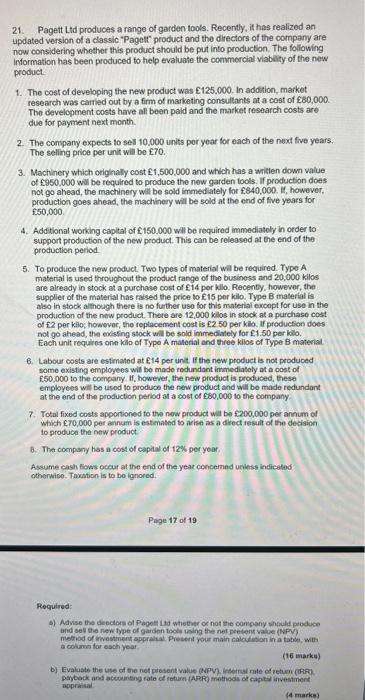

21. Pagett Ltd produces a range of garden tools. Recently, it has realized an updated version of a classic "Pagelt" product and the directors of the company are now considering whether this product should be put into production. The following information has been produced to help evaluate the commercial viability of the new product. 1. The cost of developing the new product was 125,000. In addition, market research was carrled out by a firm of marketing consultants at a cost of 80,000. The development costs have all been paid and the market research costs are due for payment next month. 2. The convany expects to sell 10,000 units por year for each of the next five years. The selling price per unit will be E7O. 3. Machinery which originally cost 1,500,000 and which has a written down value of $950,000 will be required to produce the new garden tools. If production does not go ahead, the machinery will be sold immedlately for f840,000. It, however, production goes ahead, the machinery will be sold at the end of five years for f.50,000. 4. Additional working capital of 150,000 will be required immediatoly in order to support production of the new product. This can be released at the end of the production period. 5. To produce the new product. Two types of material wal be required. Type A material is used throughout the product range of the businoss and 20,000 kilos are already in stock at a purchase cost of 214 per killo. Recenty, howewer, the supplier of the material has mised the price to E15 per kilo. Type B material is also in stock although there is no further uso for this material excopt for use in the production of the now product. There are 12,000 kilos in stock at a purchase cost of E2 per kilo; howevor, the replacement cost is 2.50 per kila. If production does not go ahead, the exisfing stock will be sold immediately for E1.50 per kilo. Each unit requires one kilo of Typo A material and threo kilos of Type B material 6. Labour costs are estimated at E14 per unit if the new product is not produced some existing employees will be mado redundant immediately at a cost of f.50,000 to the company. If, however, the new product is produced, these employees will be usod to produce the new product and will be made redundant at the end of the production period at a cost of 680,000 to the company. 7. Total fixed costs apportioned to the new product wal be fe200,000 per annum of which 70,000 per annum is estimated to arise as a drect result of the decision fo produce the new product. 0. The company has a cost of capital of 12% per yoar. Assume cash fows occur at the end of the year concerned unkess indicated otherwise. Taxation is to bo ignored. Page 17 of 19 Required: a colums for esch year: (16 marku) appratisal