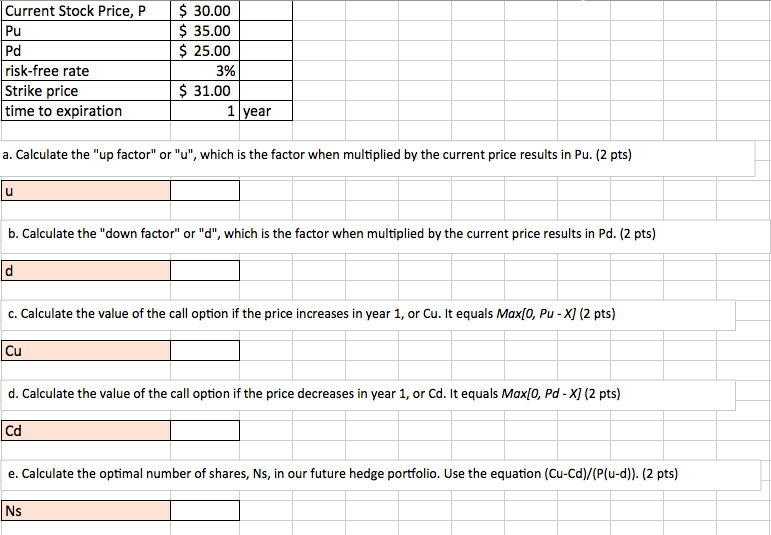

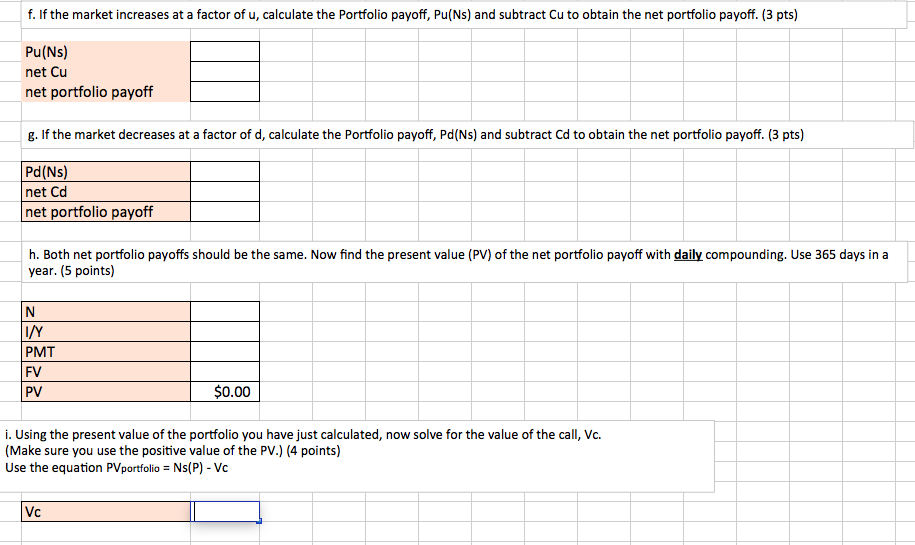

Current Stock Price, P Pu Pd risk-free rate Strike price time to expiration $ 30.00 $ 35.00 $ 25.00 3% $31.00 1 year a. Calculate the "up factor" or "u", which is the factor when multiplied by the current price results in Pu. (2 pts) u b. Calculate the "down factor" or "d", which is the factor when multiplied by the current price results in Pd. (2 pts) d c. Calculate the value of the call option if the price increases in year 1, or Cu. It equals Max[0, Pu - X] (2 pts) Cu d. Calculate the value of the call option if the price decreases in year 1, or Cd. It equals Max[0, Pd - X] (2 pts) Cd e. Calculate the optimal number of shares, Ns, in our future hedge portfolio. Use the equation (Cu-Cd)/(Plu-d)). (2 pts) Ns f. If the market increases at a factor of u, calculate the Portfolio payoff, Pu(Ns) and subtract Cu to obtain the net portfolio payoff. (3 pts) Pu(Ns) net Cu net portfolio payoff g. If the market decreases at a factor of d, calculate the Portfolio payoff, Pd(Ns) and subtract Cd to obtain the net portfolio payoff. (3 pts) Pd(Ns) net Cd net portfolio payoff h. Both net portfolio payoffs should be the same. Now find the present value (PV) of the net portfolio payoff with daily compounding. Use 365 days in a year. (5 points) N 1/Y PMT FV PV $0.00 i. Using the present value of the portfolio you have just calculated, now solve for the value of the call, Vc. (Make sure you use the positive value of the PV.) (4 points) Use the equation PVportfolio = Ns(P) - Vc Vc Current Stock Price, P Pu Pd risk-free rate Strike price time to expiration $ 30.00 $ 35.00 $ 25.00 3% $31.00 1 year a. Calculate the "up factor" or "u", which is the factor when multiplied by the current price results in Pu. (2 pts) u b. Calculate the "down factor" or "d", which is the factor when multiplied by the current price results in Pd. (2 pts) d c. Calculate the value of the call option if the price increases in year 1, or Cu. It equals Max[0, Pu - X] (2 pts) Cu d. Calculate the value of the call option if the price decreases in year 1, or Cd. It equals Max[0, Pd - X] (2 pts) Cd e. Calculate the optimal number of shares, Ns, in our future hedge portfolio. Use the equation (Cu-Cd)/(Plu-d)). (2 pts) Ns f. If the market increases at a factor of u, calculate the Portfolio payoff, Pu(Ns) and subtract Cu to obtain the net portfolio payoff. (3 pts) Pu(Ns) net Cu net portfolio payoff g. If the market decreases at a factor of d, calculate the Portfolio payoff, Pd(Ns) and subtract Cd to obtain the net portfolio payoff. (3 pts) Pd(Ns) net Cd net portfolio payoff h. Both net portfolio payoffs should be the same. Now find the present value (PV) of the net portfolio payoff with daily compounding. Use 365 days in a year. (5 points) N 1/Y PMT FV PV $0.00 i. Using the present value of the portfolio you have just calculated, now solve for the value of the call, Vc. (Make sure you use the positive value of the PV.) (4 points) Use the equation PVportfolio = Ns(P) - Vc Vc