Question

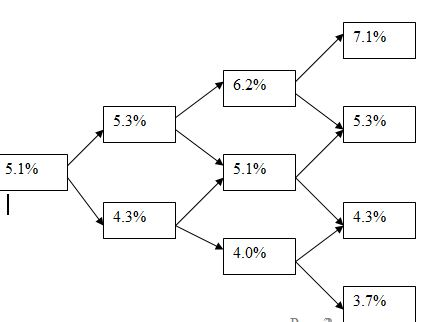

D. Consider 6-month spot interest rates evolving in the following three-step binomial tree over 24 months, i.e., with 6 months in each of the next

D. Consider 6-month spot interest rates evolving in the following three-step binomial tree over 24 months, i.e., with 6 months in each of the next three steps. The current 18-month spot interest rate is 5.15%, the current 12-month spot interest rate is 5.3%, and the current 24-month spot interest rate is 5.45%. This three-step problem involves calculation of just the third step,Find the following by assuming monthly compounding.

16. The risk neutral probability for the up move in the last (third) step.

17. The current fair value of a 18-month European call option with a strike price of $974 written on a 24-month zero coupon bond with face value $1000.

18. The current fair value of a 12-month European put option with a strike price of $994 written on a 24-month zero coupon bond with face value $1000.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Campaign Finance Reform

Authors: Melissa M. Smith, Glenda C. Williams, Larry Powell, Gary A. Copeland

1st Edition

0739145657, 978-0739145654