Answered step by step

Verified Expert Solution

Question

1 Approved Answer

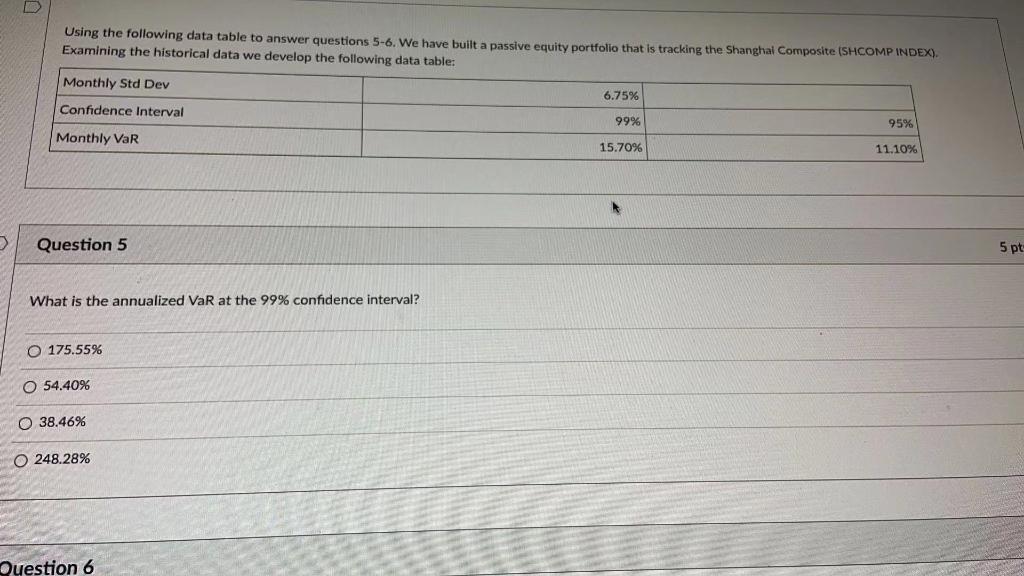

D Using the following data table to answer questions 5-6. We have built a passive equity portfolio that is tracking the Shanghal Composite (SHCOMP INDEX).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Guide To Investing In Rental Properties

Authors: Dennis Mulongo

1st Edition

979-8424909191