Answered step by step

Verified Expert Solution

Question

1 Approved Answer

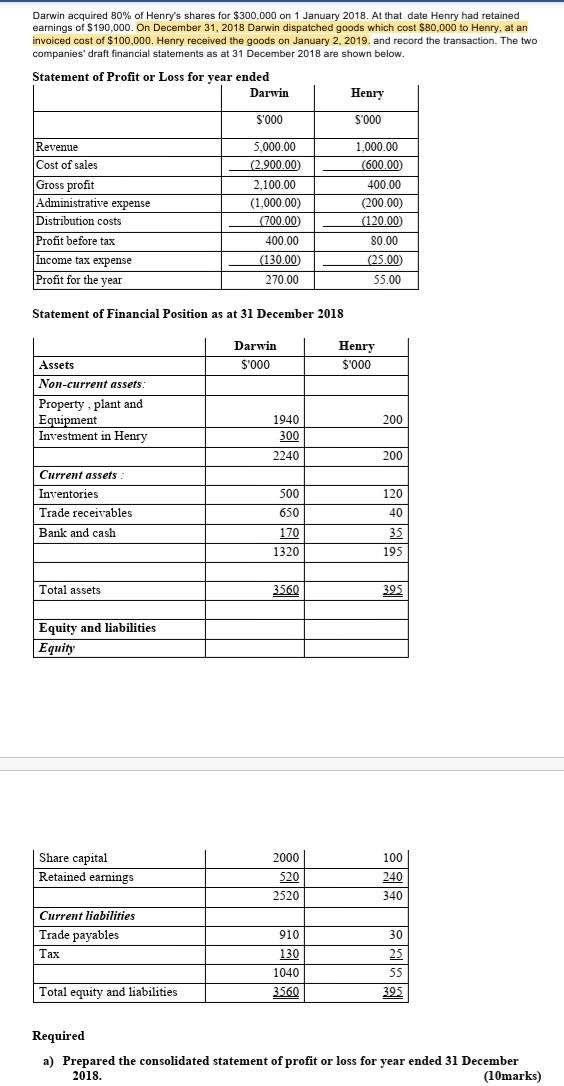

Darwin acquired 80% of Henry's shares for $300.000 on 1 January 2018. At that date Henry had retained earnings of $190,000. On December 31, 2018

Darwin acquired 80% of Henry's shares for $300.000 on 1 January 2018. At that date Henry had retained earnings of $190,000. On December 31, 2018 Darwin dispatched goods which cost $80,000 to Henry, at an invoiced cost of $100.000. Henry received the goods on January 2, 2019. and record the transaction. The two companies' draft financial statements as at 31 December 2018 are shown below. Statement of Profit or Loss for year ended Darwin Henry $'000 S'000 Revenue Cost of sales Gross profit Administrative expense Distribution costs Profit before tax Income tax expense Profit for the year 5,000.00 (2.900.00 2,100.00 (1,000.00) (700.00) 400.00 (130.00 270.00 1,000.00 (600.00 400.00 (200.00) (120.00 80.00 25.00 55.00 Statement of Financial Position as at 31 December 2018 Darwin $'000 Henry S'000 Assets Non-current assets: Property, plant and Equipment Investment in Henry 200 1940 300 2240 200 500 Current assets : Inventories Trade receivables Bank and cash 120 40 650 170 35 195 1320 Total assets 3560 395 Equity and liabilities Equity 100 Share capital Retained earnings 2000 520 2520 240 340 Current liabilities Trade payables Tax 910 130 1040 3560 30 25 55 Total equity and liabilities 395 Required a) Prepared the consolidated statement of profit or loss for year ended 31 December 2018. (10marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: John J. Wild, Ken W. Shaw

2010 Edition

9789813155497, 73379581, 9813155493, 978-0073379586