Answered step by step

Verified Expert Solution

Question

1 Approved Answer

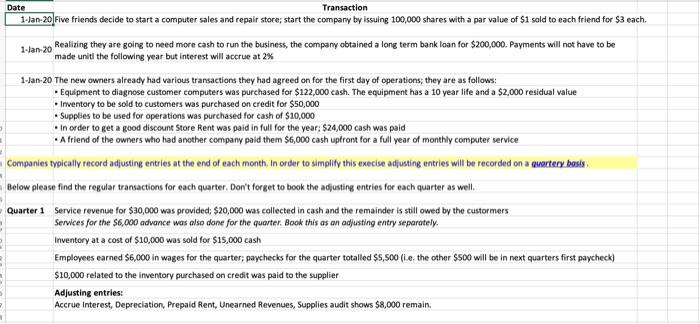

Date Transaction 1-Jan-20Five friends decide to start a computer sales and repair store; start the company ty issuing 100,000 shares with a par value of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cloud Security Auditing

Authors: Suryadipta Majumdar, Taous Madi, Yushun Wang, Azadeh Tabiban, Momen Oqaily, Amir Alimohammadifar, Yosr Jarraya, Makan Pourzandi, Lingyu Wang, Mourad Debbabi

1st Edition

3030231305, 978-3030231309