Answered step by step

Verified Expert Solution

Question

1 Approved Answer

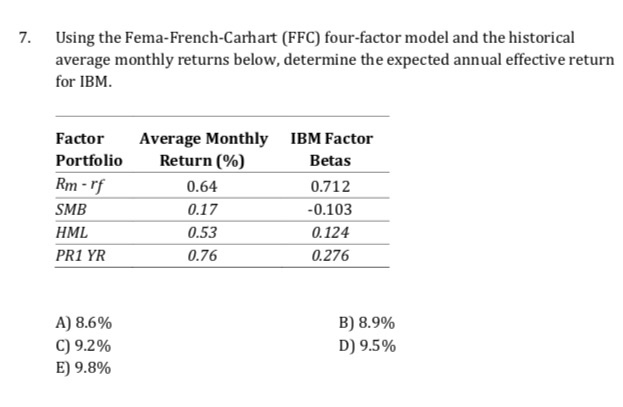

Derivatives Markets 7. Using the Fema-French-Carhart (FFC) four-factor model and the historical average monthly returns below, determine the expected annual effective return for IBM. Factor

Derivatives Markets

7. Using the Fema-French-Carhart (FFC) four-factor model and the historical average monthly returns below, determine the expected annual effective return for IBM. Factor Portfolio Rm -rf SMB HML PR1 YR Average Monthly IBM Factor Return (%) Betas 0.64 0.712 0.17 -0.103 0.53 0.124 0.76 0.276 A) 8.6% C) 9.2% E) 9.8% B) 8.9% D) 9.5% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing The Audit Function A Corporate Audit Department Procedures Guide

Authors: Michael P. Cangemi

2nd Edition

0471012556, 978-0471012559