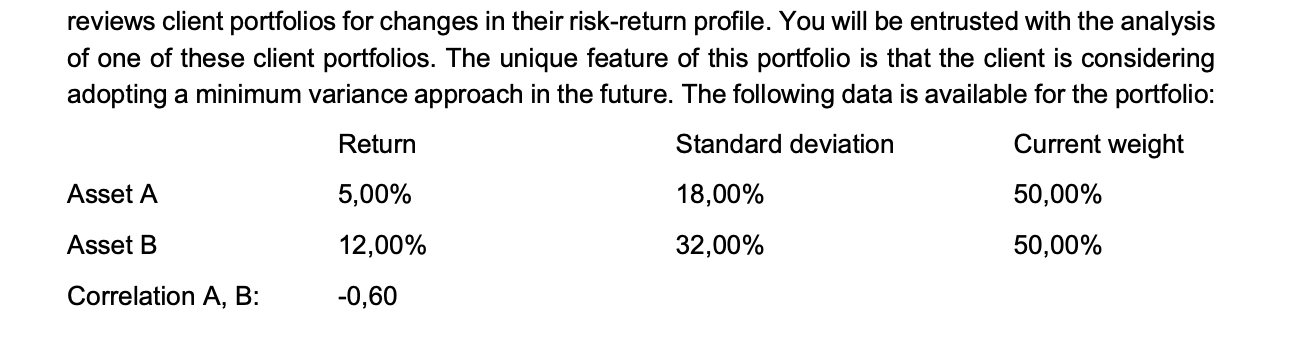

Question

Determine the weighting of the two portfolio assets that would result in the minimum risk of the portfolios. Round your results to whole percentages and

-

Determine the weighting of the two portfolio assets that would result in the minimum risk of the portfolios. Round your results to whole percentages and determine the difference in yield compared to the current weighting.

-

- The client might be willing to deviate from the minimum variance portfolio weighting by +10% or -10% respectively if this would result in a maximum 1% increase in risk. Based on this information, what allocation would you suggest? Explain your recommendation.

-

- Discuss different ways to measure the performance of the portfolio and make a proposal for the specific case based on this.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Challenging Global Finance

Authors: Elizabeth Friesen

2012th Edition

0230348793, 978-0230348790