Answered step by step

Verified Expert Solution

Question

1 Approved Answer

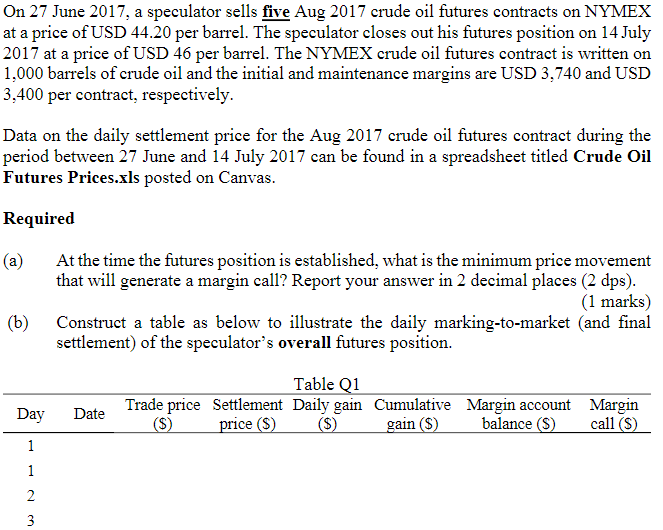

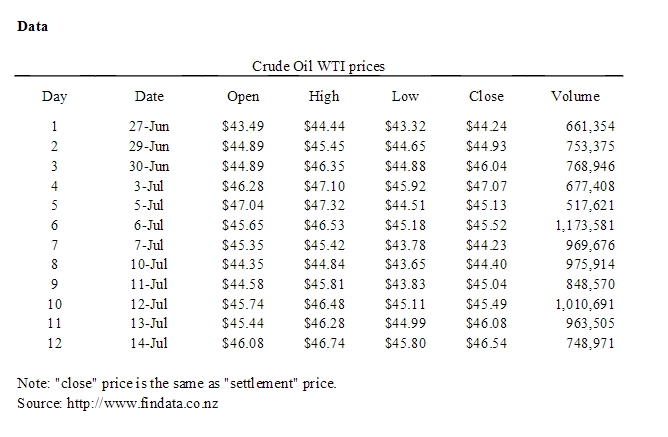

Dont answer this question in handwriting please On 27 June 2017, a speculator sells five Aug 2017 crude oil futures contracts on NYMEX at a

Dont answer this question in handwriting please

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Working Papers Chapters 1 14 For Warren Jones Tayler S Financial And Managerial Accounting

Authors: Carl S. Warren ,Jefferson P. Jones ,William Tayler

16th Edition

0357714113, 978-0357714119