Answered step by step

Verified Expert Solution

Question

1 Approved Answer

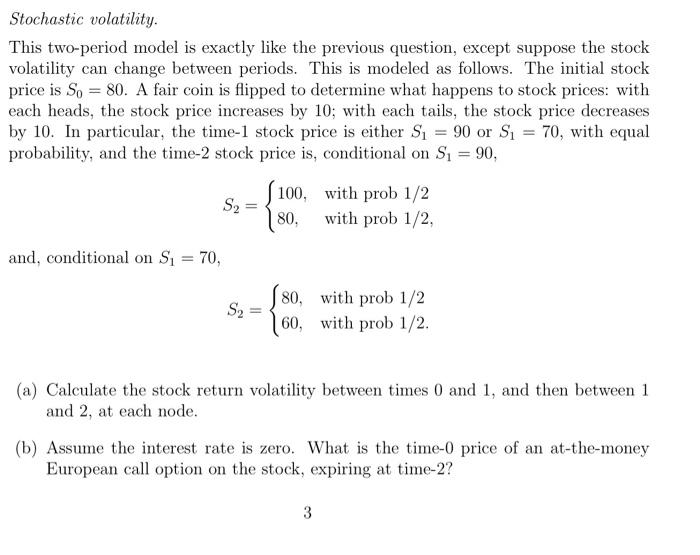

don't need other information Stochastic volatility. This two-period model is exactly like the previous question, except suppose the stock volatility can change between periods. This

don't need other information

Stochastic volatility. This two-period model is exactly like the previous question, except suppose the stock volatility can change between periods. This is modeled as follows. The initial stock price is So = 80. A fair coin is flipped to determine what happens to stock prices: with each heads, the stock price increases by 10; with each tails, the stock price decreases by 10. In particular, the time-1 stock price is either Si = 90 or Si = 70, with equal probability, and the time-2 stock price is, conditional on S1 = 90, S2 100, with prob 1/2 180, with prob 1/2, and, conditional on Si = 70, S2 80, with prob 1/2 60, with prob 1/2. (a) Calculate the stock return volatility between times 0 and 1, and then between 1 and 2, at each node. (b) Assume the interest rate is zero. What is the time-0 price of an at-the-money European call option on the stock, expiring at time-2? 3 Stochastic volatility. This two-period model is exactly like the previous question, except suppose the stock volatility can change between periods. This is modeled as follows. The initial stock price is So = 80. A fair coin is flipped to determine what happens to stock prices: with each heads, the stock price increases by 10; with each tails, the stock price decreases by 10. In particular, the time-1 stock price is either Si = 90 or Si = 70, with equal probability, and the time-2 stock price is, conditional on S1 = 90, S2 100, with prob 1/2 180, with prob 1/2, and, conditional on Si = 70, S2 80, with prob 1/2 60, with prob 1/2. (a) Calculate the stock return volatility between times 0 and 1, and then between 1 and 2, at each node. (b) Assume the interest rate is zero. What is the time-0 price of an at-the-money European call option on the stock, expiring at time-2? 3 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial And Insurance Formulas

Authors: Tomas Cipra

2010th Edition

3790829013, 978-3790829013