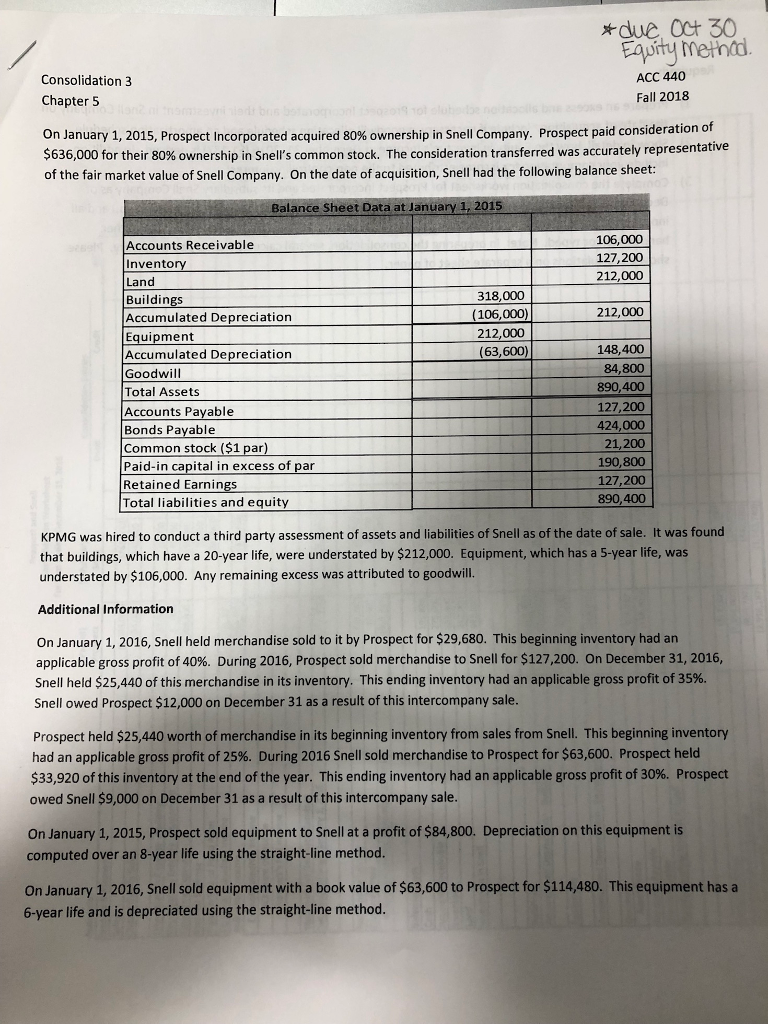

due oct 30 ACC 440 Fall 2018 Consolidation 3 Chapter 5 of On January 1, 2015, Prospect Incorporated acquired 80% ownership in Snell Company. Prospect paid consideration $636,000 for their 80% ownership in Snell's common stock. The consideration transferred was accurately representative of the fair market value of Snell Company. On the date of acquisition, Snell had the following balance sheet: Balance Sheet Data at January 1, 2015 106,000 127,200 212,000 Accounts Receivable Inventor Land Buildings Accumulated Depreciation Equipment Accumulated Depreciation Goodwill Total Assets Accounts Payable Bonds Payable Common stock ($1 par) Paid-in capital in excess of par Retained Earnings Total liabilities and equity 318,000 (106,000 212,000 (63,600) 212,000 148,400 84,800 890,400 127,200 424,000 21,200 190,800 127,200 890,400 KPMG was hired to conduct a third party assessment of assets and liabilities of Snell as of the date of sale. It was found that buildings, which have a 20-year life, were understated by $212,000. Equipment, which has a 5-year life, was understated by $106,000. Any remaining excess was attributed to goodwill. Additional Information On January 1, 2016, Snell held merchandise sold to it by Prospect for $29,680. This beginning inventory had an applicable gross profit of 40%. During 2016, Prospect sold merchandise to Snell for $127,200. On December 31, 2016, Snell held $25,440 of this merchandise in its inventory. This ending inventory had an applicable gross profit of 35%. Snell owed Prospect $12,000 on December 31 as a result of this intercompany sale Prospect held $25,440 worth of merchandise in its beginning inventory from sales from Snell. This beginning inventory had an applicable gross profit of 25%. During 2016 Snell sold merchandise to Prospect for $63,600. Prospect held $33,920 of this inventory at the end of the year. This ending inventory had an applicable gross profit of 30%. Prospect owed Snell $9,000 on December 31 as a result of this intercompany sale. On January 1, 2015, Prospect sold equipment to Snell at a profit of $84,800. Depreciation on this equipment is computed over an 8-year life using the straight-line method. On January 1, 2016, Snell sold equipment with a book value of $63,600 to Prospect for $114,480. This equipment has a 6-year life and is depreciated using the straight-line method. due oct 30 ACC 440 Fall 2018 Consolidation 3 Chapter 5 of On January 1, 2015, Prospect Incorporated acquired 80% ownership in Snell Company. Prospect paid consideration $636,000 for their 80% ownership in Snell's common stock. The consideration transferred was accurately representative of the fair market value of Snell Company. On the date of acquisition, Snell had the following balance sheet: Balance Sheet Data at January 1, 2015 106,000 127,200 212,000 Accounts Receivable Inventor Land Buildings Accumulated Depreciation Equipment Accumulated Depreciation Goodwill Total Assets Accounts Payable Bonds Payable Common stock ($1 par) Paid-in capital in excess of par Retained Earnings Total liabilities and equity 318,000 (106,000 212,000 (63,600) 212,000 148,400 84,800 890,400 127,200 424,000 21,200 190,800 127,200 890,400 KPMG was hired to conduct a third party assessment of assets and liabilities of Snell as of the date of sale. It was found that buildings, which have a 20-year life, were understated by $212,000. Equipment, which has a 5-year life, was understated by $106,000. Any remaining excess was attributed to goodwill. Additional Information On January 1, 2016, Snell held merchandise sold to it by Prospect for $29,680. This beginning inventory had an applicable gross profit of 40%. During 2016, Prospect sold merchandise to Snell for $127,200. On December 31, 2016, Snell held $25,440 of this merchandise in its inventory. This ending inventory had an applicable gross profit of 35%. Snell owed Prospect $12,000 on December 31 as a result of this intercompany sale Prospect held $25,440 worth of merchandise in its beginning inventory from sales from Snell. This beginning inventory had an applicable gross profit of 25%. During 2016 Snell sold merchandise to Prospect for $63,600. Prospect held $33,920 of this inventory at the end of the year. This ending inventory had an applicable gross profit of 30%. Prospect owed Snell $9,000 on December 31 as a result of this intercompany sale. On January 1, 2015, Prospect sold equipment to Snell at a profit of $84,800. Depreciation on this equipment is computed over an 8-year life using the straight-line method. On January 1, 2016, Snell sold equipment with a book value of $63,600 to Prospect for $114,480. This equipment has a 6-year life and is depreciated using the straight-line method