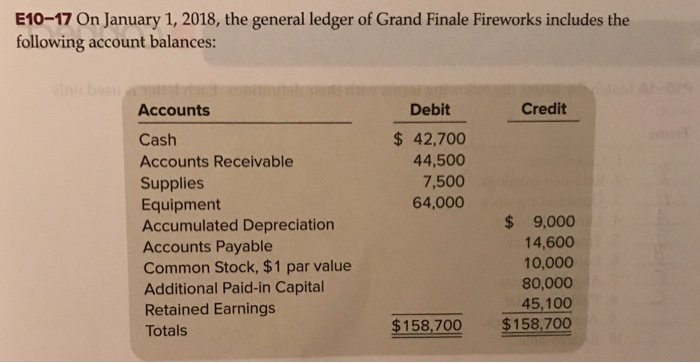

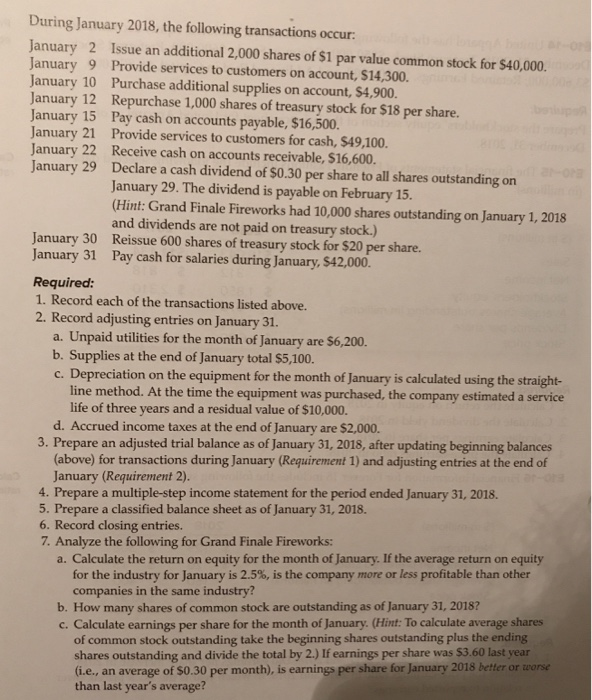

E10-17 On January 1, 2018, the general ledger of Grand Finale Fireworks includes the following account balances: Debit Credit Accounts $42,700 44,500 7,500 64,000 Cash Accounts Receivable Supplies Equipment Accumulated Depreciation Accounts Payable Common Stock, $1 par value Additional Paid-in Capital Retained Earnings Totals $ 9,000 14,600 10,000 80,000 45,100 $158,700 $158,700 During January 2018, the following transactions occur January 2 Issue an additional 2,000 shares of $1 par value common stock for $40,000. January 9 Provide services to customers on account, $14,300. January 10 Purchase additional supplies on account, $4,900. January 12 Repurchase 1,000 shares of treasury stock for $18 per share. January 15 Pay cash on accounts payable, $16,500 January 21 Provide services to customers for cash, $49,100. January 22 Receive cash on accounts receivable, $16,600 January 29 Declare a cash dividend of $0.30 per share to all shares outstanding on January 29. The dividend is payable on February 15. Hint: Grand Finale Fireworks had 10,000 shares outstanding on January 1, 2018 and dividends are not paid on treasury stock.) January 30 Reissue 600 shares of treasury stock for $20 per share. January 31 Pay cash for salaries during January, $42,000. Required 1. Record each of the transactions listed above. 2. Record adjusting entries on January 31. a. Unpaid utilities for the month of January are $6,200. b. Supplies at the end of January total $5,100. c. Depreciation on the equipment for the month of January is calculated using the straight- line method. At the time the equipment was purchased, the company estimated a service life of three years and a residual value of $10,000. d. Accrued income taxes at the end of January are $2,000. 3. Prepare an adjusted trial balance as of January 31, 2018, after updating beginning balances (above) for transactions during January (Requirement 1) and adjusting entries at the end of January (Requirement 2). 4. Prepare a multiple-step income statement for the period ended January 31, 2018. 5. Prepare a classified balance sheet as of January 31, 2018. 6. Record closing entries. 7. Analyze the following for Grand Finale Fireworks: a. Calculate the return on equity for the month of January. If the average return on equity for the industry for January is 2.5%, is the company more or less profitable than other companies in the same industry? b. How many shares of common stock are outstanding as of January 31, 2018? c. Calculate earnings per share for the month of January. (Hint:To calculate average shares of common stock outstanding take the beginning shares outstanding plus the endi shares outstanding and divide the total by 2.) If earnings per share was $3.60 last year (i.e., an average of $0.30 per month), is earnings per share for January 2018 than last year's average