Answered step by step

Verified Expert Solution

Question

1 Approved Answer

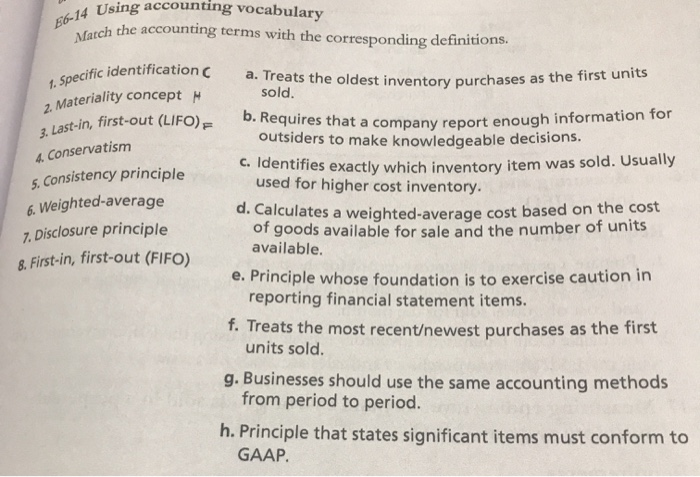

E6-14 Usin 4 Using accounting vocabulary carch the accounting terms with the corresponding definitions. Specific identification 2. Materiality concept 2. Last-in, first-out (LIFO) 4. Conservatism

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Financial Accounting

Authors: Thomas Beechy, Umashanker Trivedi, Kenneth MacAulay

6th edition

013703038X, 978-0137030385