Answered step by step

Verified Expert Solution

Question

1 Approved Answer

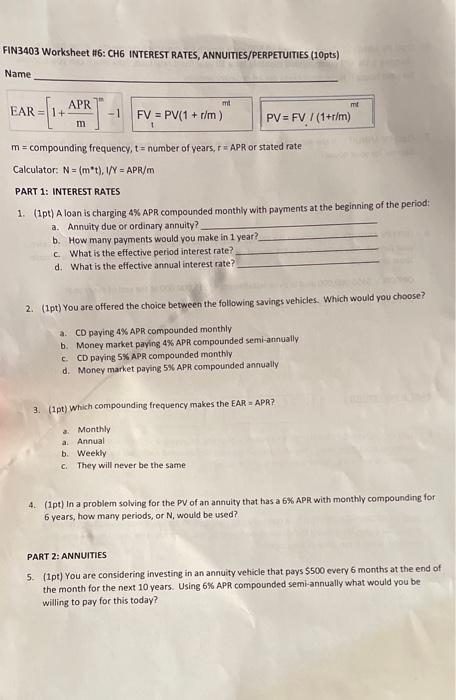

EAR=[1+mAPR]m1FV=iV(1+r/m)m/PV=FV1I(1+r/m)mt m= compounding frequency, t= number of years, r=APR or stated rate Calculator: N=(mt),1/Y=APR/m PART 1: INTEREST RATES 1. (1pt) A loan is charging 4%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance An Integrated Planning Approach

Authors: Ralph R Frasca

8th edition

136063039, 978-0136063032