Introduction Early one morning in March, Jordan Buford was preparing his daily work when his boss, Olivia Anton, approached him and announced, Little Annin Flagmakers

Introduction

Early one morning in March, Jordan Buford was preparing his daily work when his boss, Olivia Anton, approached him and announced, “Little Annin Flagmakers (LAF) has submitted an application for a line of credit (LOC) for April through June. I want you to prepare budgeted financial statements similar to the ones you prepared for our last LOC application. I need this by 3 p.m. today for the 4 p.m. credit committee meeting. Be prepared to make a loan recommendation and to address questions from the credit committee. I have cleared your schedule. Let me know if you need anything.” Kent Bank is a state bank with multiple branches that offers a variety of services for personal and commercial needs. The bank has been serving the local community for more than 110 years and prides itself on its personalized approach to provide financial services, local management, long-term stability, and a full range of deposit and lending products and services. Commercial credit decisions at Kent Bank are made by the Commercial Credit Committee, which consists of the senior commercial credit analyst and two vice presidents. Buford was recently hired by Kent Bank as a commercial analyst to provide analysis for commercial loan applications. During his undergraduate studies, he studies accounting and finance, and shortly after graduation passed the CMA (Certified Management Accountant) examination. Buford reports directly to Anton, the senior commercial credit analyst who has been with Kent Bank for 10 years. As Buford began the work, he recalled his last LOC analysis and how well received it was. He had taken the information provided by the company and developed master budgets in Excel that used an input section with numbers that could be changed for assessing different scenarios. The committee had specifically asked about the effect of a sales reduction of 2%, 5%, and 10% on the applicant’s cash needs. He wanted to be prepared for these types of questions.

Little Annin Flagmakers Background

LAF manufactures one product, a large durable 8’×12’ American flag, which it sells for $120. Because of the large size of the flag, this product is not sold in stores; rather it is sold through a relatively small number of online retailers. Each quarter, retailers estimate sales for the upcoming five months, revising proximate sales as necessary. In general, the retailers are reasonably good at estimating their sales needs, but some variation in demand does occur, and the retailers expect to be able to adjust orders as needed. LAF allows retailers to adjust each month’s purchases to 80% to 120% of the estimated sales levels. Flags are shipped to retail customers using JIT distribution so that the online retailers do not have to store inventory. Typical sales for the flag are 1,800 units per month with seasonal increases in April through August. Sales estimates are 2,500 units in April, 6,000 units in May, 3,000 units in June, 2,500 units in July, and 2,000 units in August. Customers historically have paid 40% of their purchases in the month of the sale, 55% in the following month, and the remaining 5% is uncollectible.

Manufacturing and SG & A costs

The flags are made in one plant, which has a capacity of 6,200 flags per month. LAF budgets have 20% of next month’s sales in finished goods inventory at the end of each month. There is plenty of storage space for finished goods. Fabric is the only direct materials and each flag requires five pounds of fabric at $7 per pound. LAF plans to have 40% of next month’s fabric needs on hand at the end of the month. Fabric is purchased on credit with 40% paid in the month of purchase and 60% paid the next month. The standard direct labor hours to manufacture one flag is 0.50 hours at $40 per hour. For simplicity, direct labor costs are budgeted as if they were paid when incurred. Manufacturing overhead rates are computed quarterly and applied based on direct labor hours. Fixed manufacturing overhead costs are estimated to be $57,950 per month, of which $20,000 is property, plant, and equipment (PPE) depreciation. Variable manufacturing overhead, including indirect materials, indirect labor, and other costs, is estimated at $10 per direct labor hour. The selling and administrative expenses include variable selling costs (primarily shipping) of $1.25 per unit and fixed costs of $63,000 per month, of which $10,000 is depreciation of the administrative office building and equipment.

Financial statement details and cash planning

LAF uses first in, first out (FIFO) inventory valuation. As of March 31, the expected finished goods inventory is 410 units, valued at $75 per unit. The company expects to have 4,600 pounds of fabric on hand, valued at $7 per pound. Other expected account balances include accounts payable at $55,000, accounts receivable at $132,000, cash at $37,745, land at $520,000, and building and equipment at $1,800,000 with accumulated depreciation of $750,000. LAF has no long-term debt; common stock is valued at $500,000 and is not expected to change during the quarter; expected retained earnings as of March 31 are $1,247,695. LAF budgets for $30,000 ending cash balance each month and is requesting a line of credit that will allow it to adjust for its cash needs. The dividends of $15,000 are paid each month. During the quarter, LAF planned to purchase equipment in May and June for $47,820 and $154,600, respectively. This equipment is being purchased to increase capacity and is not expected to come on line until after the quarter, thus not affecting the manufacturing overhead costs.

Loan details

LAF has requested a line of credit of $60,000 to cover production costs during the seasonal increase in business. Kent Bank uses the following terms of its lines of credit. All borrowing is done at the beginning of the month in whole dollar increments. All repayments are made at the end of the month in whole dollar increments. The full line of credit is expected to be paid off by the end of the quarter with all the interest repaid at the end of the quarter. The interest rate on this loan is 16% per year.

Requirements:

1. Using the data input provided (Exhibit 1), prepare LAF’s master budgets in Excel. Do not hard-code numbers into the spreadsheet, except in the financing section of the cash budget.

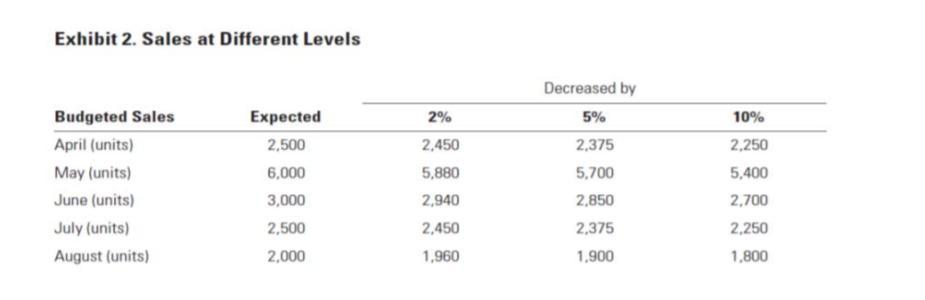

2. Conduct a sensitivity analysis, decreasing sales 2%, 5%, and 10% for April through August. New sales levels are provided in Exhibit 2. Adjust the financing and cash needs at these new sales levels.

3. Determine a credit recommendation for Kent Bank, to lend or not.

-------------------------------------------

QUESTION:

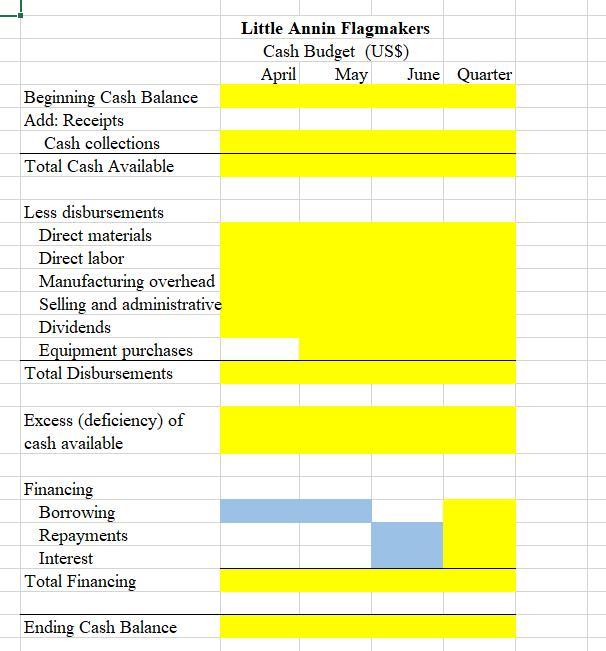

Complete cash budget

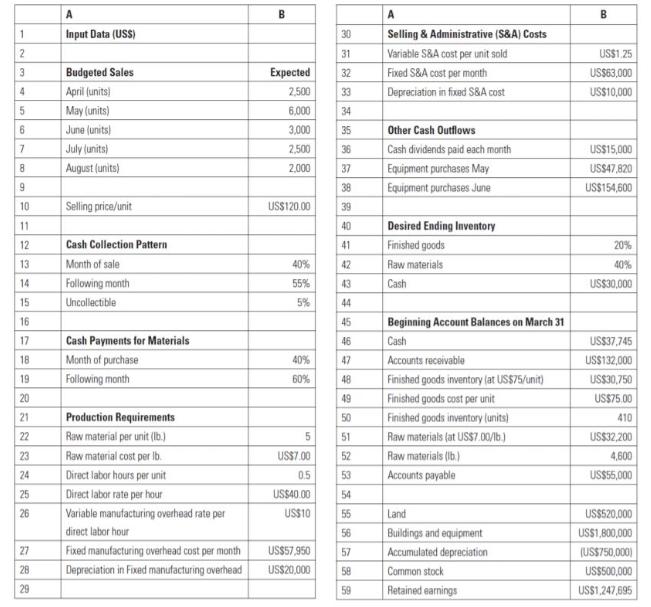

A A B 1. Input Data (USS) 30 Selling & Administrative (S&A) Costs 31 Variable S&A cost per unit sold US$1,25 3 Budgeted Sales Expected 32 Fixed S&A cost per month US$63,000 April (units) Depreciation in fixed S&A cost 4. 2,500 33 US$10,000 May (units) 6,000 34 June (units) 3,000 35 Other Cash Outflows July (units) 2,500 36 Cash dividends paid each month US$15,000 8 August (units) 2,000 37 Equipment purchases May USS47,820 Equipment purchases June US$154,600 38 10 Selling price/unit US$120.00 39 Desired Ending Inventory 11 40 12 Cash Collection Pattern 41 Finished goods 20% Month of sale Following month Uncollectible 13 40% 42 Raw materials 40% 14 55% 43 Cash US$30,000 15 5% 44 16 45 Beginning Account Balances on March 31 17 Cash Payments for Materials 46 Cash US$37,745 Month of purchase Following month 18 40% 47 Accounts recoivable US$132,000 60% Finished goods inventory lat US$75/unit) US$30,750 19 48 20 49 Finished goods cost per unit USS75.00 21 Production Requirements 50 Finished goods inventory (units) 410 22 Raw material per unit (b.) 51 Raw materials (at USS7.00/b.) US$32,200 23 Raw material cost per Ib. USS7.00 52 Raw materials (Ib.) 4,600 Diract labor hours per unit Direct labor rate per hour 24 0.5 53 Accounts payable USS55,000 25 USS40.00 54 26 Variable manutacturing overhead rate per US$10 55 Land US$520,000 direct labor hour Buildings and equipment Accumulated depreciation 56 USS1,800,000 27 Fixed manufacturing overhead cost per month US$57,950 57 (USS750,000) 28 Depreciation in Fixed manufacturing overhead US$20,000 58 Common stock USS500,000 29 59 Retained earnings USS1,247,695

Step by Step Solution

3.45 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

Introduction Early one morning in March Jordan Buford was preparing his daily work when his boss Olivia Anton approached him and announced Little Annin Flagmakers LAF has submitted an application for ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: James A. Hall

7th Edition

978-1439078570, 1439078572